Simple Summary

This week, Gauntlet recommends no changes to Compound II’s current parameterization.

Abstract

Gauntlet’s simulation engine has ingested the latest market and liquidity data. These recommendations are Gauntlet’s regular parameter recommendations as part of Dynamic Risk Parameters and align with the Moderate risk level chosen by the Compound community.

Motivation

This set of parameter updates seeks to maintain the overall risk tolerance of the protocol while making risk trade-offs between specific assets. Gauntlet has published a blog post on our parameter recommendation methodology to provide more context to the community.

Our parameter recommendations are driven by an optimization function that balances 3 core metrics: insolvencies, liquidations, and borrow usage. Our parameter recommendations seek to optimize for this objective function. Gauntlet’s agent-based simulations use a wide array of varied input data that changes on a daily basis (including but not limited to user positions, asset volatility, asset correlation, asset collateral usage, DEX/CEX liquidity, trading volume, expected market impact of trades, liquidator behavior). Our simulations tease out complex relationships between these inputs that cannot be simply expressed as heuristics. As such, the charts and tables shown below may help understand why some of the param recs have been made but should not be taken as the only reason for recommendation. Our individual collateral pages on the dashboard cover other key statistics and outputs from our simulations that can help with understanding other interesting inputs and results related to our simulations.

Gauntlet’s simulations show that Compound is effectively balancing capital efficiency and market risk under current market conditions. As such, Gauntlet recommends no parameter changes this week.

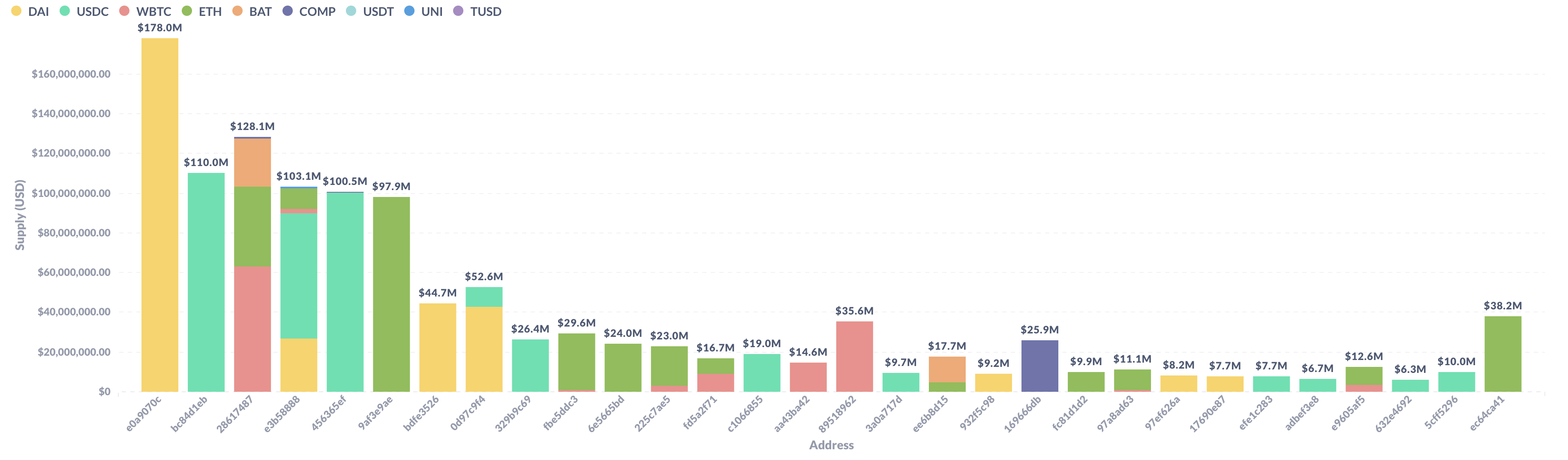

Top 30 borrowers’ aggregate positions & borrow usages

Top 30 borrowers’ entire supply

Top 30 borrowers’ entire borrows

Price changes of key assets since our last post

For most of the highly supplied assets, the underlying prices haven’t fluctuated significantly, thus resulting in fairly constant borrow usages for most of the top risky users.

Time series of Value at Risk (VaR) since our last post

We have seen VaR fluctuate since our last post, ranging from as high as $7.3M to as low as $4.9k. This is primarily due to minor underlying price fluctuations of the user with address 0xe84a061897afc2e7ff5fb7e3686717c528617487, which we noted in our last post, and continues to be right on the cutoff of being meaningfully risky (~74% borrow usage).

This user last updated their position on 9/7/2022. We recommend that this user either increase their supply or decrease their borrows such that their borrow usage is at most 65%. Otherwise, should this position become riskier, we may recommend decreasing collateral factors in some combination of {ETH, WBTC, BAT} to reduce the insolvency risk this user poses during a Black Thursday event.

Dashboard

The community should use Gauntlet’s Risk Dashboard to understand better the updated parameter suggestions and general market risk in Compound.

When making recommendations, Gauntlet takes into account the entire distribution of insolvencies and liquidations from our simulations and weighs them against increases in borrows. The below metrics give the community insight into some of the insolvency and liquidation tail risks the protocol could face and Capital Efficiency improvements the protocol stands to gain. Click the collateral-specific pages linked in the Collateral Risk section for more detailed simulation metrics.

Value at Risk represents the 95th percentile insolvency value that occurs from simulations we run over a range of volatilities to approximate a tail event.

Liquidations at Risk represents the 95th percentile liquidation volume that occurs from simulations we run over a range of volatilities to approximate a tail event.

Next Steps

Given that Gauntlet is proposing no parameter changes, no governance proposal will be created for this forum post.

By approving this proposal, you agree that any services provided by Gauntlet shall be governed by the terms of service available at gauntlet.network/tos.

Quick Links

Analytics Dashboard

Risk Dashboard

Gauntlet Parameter Recommendation Methodology

Gauntlet Model Methodology