Background

Block Analitica is the core entity behind MakerDAO’s risk team. Our mandate includes monitoring Maker portfolio risk profile and to proactively provide solutions to mitigate and/or minimize financial risk exposure. With the increasing direct integration with other protocols, especially secondary lenders such as Compound, it is becoming more important for us to have a better overview of the systemic DeFi risk. D3M integration with Aave is in production with an already significant exposure of almost 300M. This has provided a new challenge for our team to tackle (risk dashboard).

Additionally, as most likely well known within the Compound community, the Compound D3M integration is high on the priority list for the Maker core units to implement. For this reason we’re actively following both protocols’ governance processes and also monitor the impact of voting decisions on user behavior.

One of the recent major decisions made by the Compound governance was to cut the COMP rewards in half. In the same proposal by @TylerEther, it was suggested to end all COMP rewards programs and only use them to kickstart new markets moving forward. It also mentioned that the proposal for cutting all rewards would happen 1 month after the initial proposal which is around April 15. Regarding this, our team recently shared some insights that might be interesting to the community.

Additionally, in our risk assessment of Compound, we learned that DAI supplied to Compound is quite safe from a financial risk perspective given that most of the exposure comes from recursive positions. There are questions that naturally arise when all of these aspects of the protocol are put together:

- How has the distribution of recursive position supply changed relative to other wallet strategies after the governance decision?

- What is the share of recursive position supply that is profitable if the rewards would decrease even further?

- How much recursive position supply would Compound lose by further dropping the rewards, assuming that users would soon close any unprofitable position? How does that value compare to the necessary spend to make the recursive position strategy profitable for the users?

These are three (sets of) questions that we aimed to answer below, based on the protocol snapshot on April 7th.

Summary

Given a 50% drop in COMP rewards, executed on March 26th, we haven’t seen a corresponding drop in supply of wallets categorized as Recursive Positions. Currently, ⅓ of supply comes from Recursive Positions and after the drop, ¾ of that supply is contributed by unprofitable positions. If rewards would drop to zero, 97% of total supply of 3.31B could be closed due to unprofitable Recursive Positions. What share of that would happen in practice can only be a guesstimate but given the before/after 50% drop in rewards, that hasn’t happened as much as we expected. Partial explanation for this is that even if wallets tend to have Recursive Position as the dominant wallet strategy, they still sometimes hold a non-negligible amount of either ETH or WBTC. This is a positive sign for Compound governance regarding the change so far, although this doesn’t necessarily answer the question of the impact of dropping all rewards altogether which could have a much more severe impact on Compound Markets supply/TVL.

Analysis

Chart 1. Supply per Wallet Strategy

To get an overview of how the protocol user behavior changes across different segments, we categorized each of the wallets into several strategies. As it is often a gray line which strategy is being used, we chose the one that is the most dominant for a given address/wallet. For instance, a Recursive Position is defined by having at least 50% of supply and 50% of borrows in stablecoins.

While total supply during this period dropped by 700M, we can see in the below chart that the distribution between different wallet strategies hasn’t changed in a major way before and after the governance decision which was executed on March 26th. In the protocol snapshot, around 28% of wallet supply comes from Supply Only strategy, 33% from Recursive Positions and 38% from Long Positions. Less than 1% are Short Positions. Recursive Positions share of total supply dropped from 36% (March 25th) to 33% (April 7th) which is minimal. From this lack of change in distribution across different wallet strategies, we can infer that potentially unprofitable wallets identified as Recursive Positions mostly haven’t closed their positions.

Chart 2. Recursive Positions: Share of Profitable Supply per Reward Multiplier

To understand the chart below, we first need to define what the Reward Multiplier describes. Its aim is to estimate the impact on supply profitability across different relative amounts of rewards given to the protocol users. The value of 1 defines the current COMP rewards distribution setup. At the value of 2, it is the rewards distributed prior to cutting the rewards in half. The value of zero estimates the protocol state when all COMP rewards are off.

We can see that before the rewards decrease, practically all of Recursive Positions supply was profitable (at Reward Multiplier = 2). After the cut (Reward Multiplier = 1), almost ¾ of supply is unprofitable. That would increase to 97% if no rewards were distributed (Reward Multiplier = 0). This final value is not exactly 100% because of the imperfect heuristic for wallet strategy categorization.

Important consideration to reiterate on is that the wallet strategy is determined by the identified wallet’s dominant strategy. We’ve seen in practice that wallets tend to sometimes have more mixed strategies where a Recursive position is also supplying some amount of ETH and WBTC. These seem to be a minority in terms of TVL so the segmentation manages to show the big picture of wallet strategy behavior.

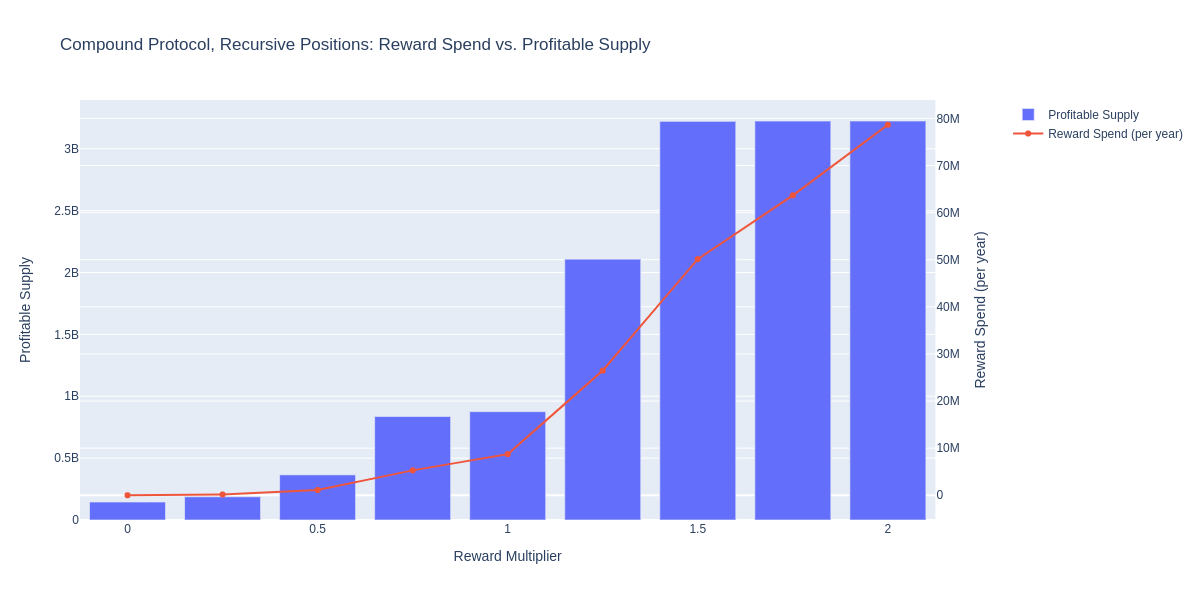

Chart 3. Recursive Positions: Reward Spend vs. Profitable Supply

The interpretation of Reward multiplier in Chart 3 is the same as in the previous chart. The only difference is that our aim is to look at how much Recursive Positions supply the protocol can potentially lose when further dropping rewards, given the assumption that all unprofitable supply positions would be closed after the governance decision. It’s a matter of guesstimates to what extent this would happen. We were able to build some intuition from Chart 1 which indicated that users haven’t shown much responsiveness to the change so far.

At a yearly spend of 79M directed at Recursive Positions, implemented before the reward cut, practically all of the current supply would be profitable, same as in the chart above. This implies the current Recursive Positions supply at 3.22B. That translates to 40 dollars in supply for each reward dollar spent.

At the current reward distribution setup, 875M is still profitable. That’s at a much lower spend of 8.7M per year if all of these were closed. That translates to 100 dollars in supply for each reward dollar spent if all unprofitable positions would close. If no rewards were distributed, there would be 145M Recursive Positions supply left, assuming that all unprofitable wallet positions would close and/or move elsewhere.

This assumption is conservative, especially given the above data showing that protocol users are not as responsive/effective at optimizing their positions (closing when they become unprofitable).

Additionally, the above spend is computed assuming a constant reward APY across different Reward Multipliers and their shares of profitable supply, not allocating an arbitrary amount of COMP tokens directed at yield farming which would incidentally change the reward APY for each Reward Multiplier (while the total amount distributed would be constant).

Conclusion

This analysis is an output of Maker Risk Team’s internal monitoring of protocols that are either integrated into Maker Protocol via D3M or are highly prioritized to be integrated soon. Governance decisions of these protocols can have a major impact on the risk profile of DAI sent into the integrated D3M smart contracts. As previously shared by our team, the expectation is that the rates would (counter-intuitively) decrease because of the unwinding of Recursive Positions supply which artificially increase the market utilization. This could in turn, if D3M was integrated, increase Maker’s DAI debt exposure on Compound (assuming the debt ceiling would not have been reached yet).

While we haven’t seen this happen yet, we’ll keep monitoring how this evolves in the coming weeks. This is especially important due to the Compound governance timeline of approximately 7 days (also mentioned in our risk assessment) if 0 COMP issuance vote is followed through around April 15.

We hope that the insights from the analysis provide some valuable support in the future decision-making relating to COMP rewards. Additionally, we encourage further discussion on this topic and are open to feedback on how to improve the above presented methodology.