As planned in an earlier forum post, we have updated our dynamic parameter methodology to include recommendations for the reserve factor, as well as our usual parameters. To outline our thinking behind this addition, we split lending parameter optimization into a two step process:

- Balancing losses due to insolvency with capital efficiency

- Balancing the tradeoff between increasing supplier APY and growing reserves to cover insolvency losses

In the first stage of our modeling, we focused on optimizing capital efficiency within the community’s acceptable risk tolerance. Our primary levers in this optimization are the Collateral Factor and Liquidation Incentive, which most importantly allow us to manage the overall Value at Risk (VaR) of the protocol. We seek to balance VaR against borrow usage, which we use as a metric for the capital efficiency of the protocol. Since losses to a lending protocol occur during insolvencies - events where collateral is unable to cover the full value of a liquidated loan - controlling the frequency and severity of such cases is key to managing the overall value at risk. Within our simulation framework, the Collateral Factor drives the likelihood of a given loan triggering its liquidation threshold. The Liquidation Incentive parameter then drives the cost of liquidating the collateral and by extension the severity of insolvency loss.

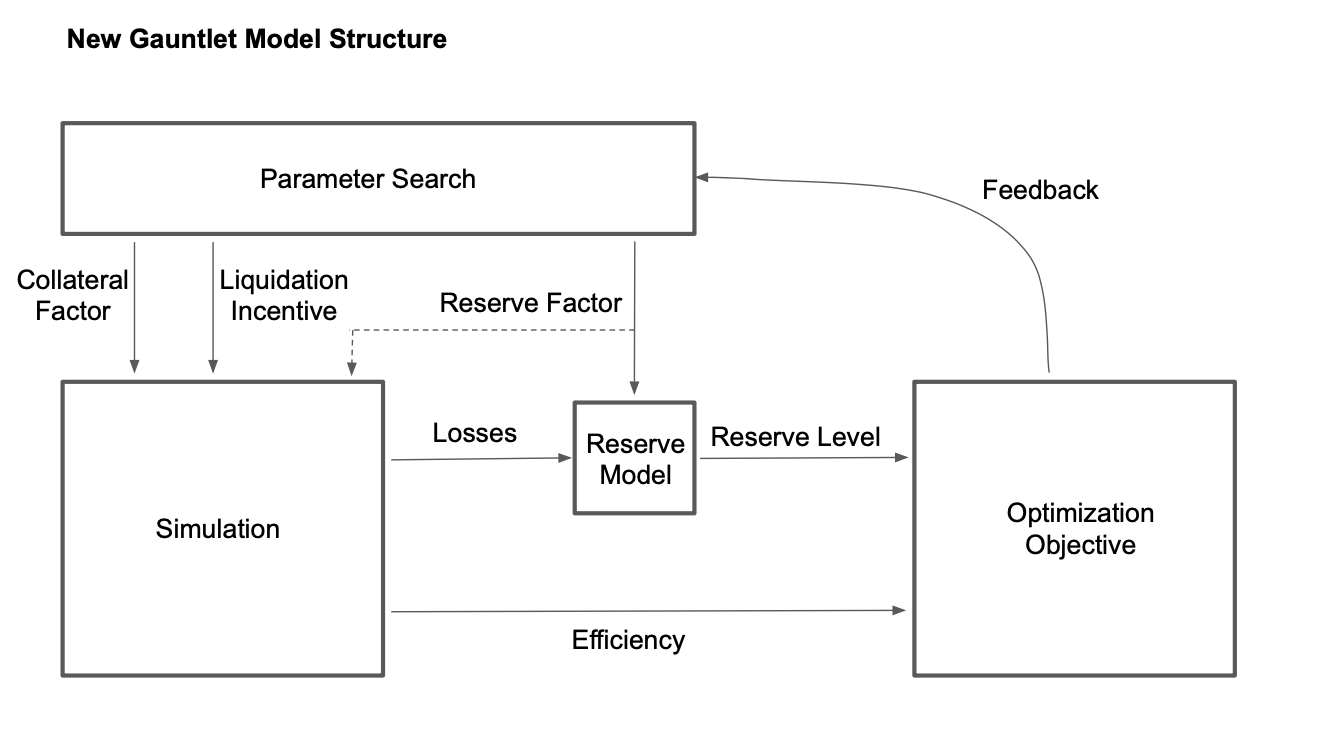

A schematic view of the first stage of our modeling process is shown in the diagram above. Starting from the top left, we search through a range of lending parameters, which serve as inputs to the simulation. The simulation output then determines the level of risk and protocol efficiency for the trial set of parameters, which are evaluated against the protocol objectives. Finally, we can adjust the input parameters based on feedback to more closely meet the objectives. Now that we have reviewed the process used so far, let’s consider how the reserve factor changes things.

How does the Reserve Factor fit in?

We are now adding a layer to the existing simulation logic that allows us to reflect the second step of lending protocol risk management: building sufficient but not excessive reserves to absorb losses that do occur. Our model assumes the protocol would like to build reserves greater than insolvency losses by a small margin, and includes this as an optimization objective. As reserves are built and losses occur in the simulation, a higher setting for the reserve factor allows us to absorb more losses while maintaining reserve coverage, while a lower setting for the reserve factor would require losses to be managed more tightly.

A schematic for the new model structure is shown above, incorporating all the existing elements of the initial model and the new reserve factor layer. This illustrates where the reserve factor fits downstream of the simulation logic and how reserves are measured against losses as a model objective. As we continue to gather data on reserve factor adjustments, we expect to also incorporate the second-order effect of the reserve factor on the simulation itself, which is shown here by the dashed line. Because setting aside reserves locks up some assets that would otherwise be available to protocol users, there may be an indirect effect on user economics and thus capital efficiency from this. To refine our model here, we plan to recommend incremental adjustments to reserve factors that will gradually move reserve growth towards protocol targets while allowing us to further study indirect effects as the data becomes available.

Our Recommendation and Reasoning

Recommendations:

We recommend decreasing reserve factors for USDC, USDT, and TUSD from 7.5% to 3.75%, and decreasing all other reserve factors by 500 bps (for example, decreasing ETH reserve factor from 20% to 15%).

Reasoning:

The one-week rolling average VaR for Compound in a Black Thursday magnitude event is $0.30M.

The protocol has an existing reserve pool of $42.87M, broken down as follows:

The protocol is expected to build reserves at a $3.86M annual rate should the reserve factors remain unchanged, broken down as follows:

Since the existing pool and growth rate are more than sufficient to cover a very severe loss event, we believe that the optimal level of reserve factors is well lower than they are currently. By implementing the recommended cuts, the protocol could reduce its estimated annual reserve growth rate from $3.86M to $2.33M, reallocating $1.53M of funds to suppliers and thus incentivizing more users to lock collateral in Compound. As we continue to improve our model, we look forward to updating the community on further progress and fine-tuning our reserve factor recommendations in a future forum post.

By approving this proposal, you agree that any services provided by Gauntlet shall be governed by the terms of service available at gauntlet.network/tos.