Simple Summary

A proposal to adjust one (1) risk parameter for one (1) Compound V2 asset.

We recommend decreasing SUSHI collateral factor from 73% to 70%. The community has aligned on a risk off framework.

Abstract

Gauntlet’s simulation engine has ingested the latest market and liquidity data. These recommendations are Gauntlet’s regular parameter recommendations as part of Dynamic Risk Parameters and align with the Moderate risk level chosen by the Compound community.

Motivation

This set of parameter updates seeks to maintain the overall risk tolerance of the protocol while making risk trade-offs between specific assets. Gauntlet has published a blog post on our parameter recommendation methodology to provide more context to the community.

Our parameter recommendations are driven by an optimization function that balances 3 core metrics: insolvencies, liquidations, and borrow usage. Our parameter recommendations seek to optimize for this objective function. Gauntlet’s agent-based simulations use a wide array of varied input data that changes on a daily basis (including but not limited to user positions, asset volatility, asset correlation, asset collateral usage, DEX/CEX liquidity, trading volume, expected market impact of trades, liquidator behavior). Our simulations tease out complex relationships between these inputs that cannot be simply expressed as heuristics. As such, the charts and tables shown below may help understand why some of the param recs have been made but should not be taken as the only reason for recommendation. Our individual collateral pages on the dashboard cover other key statistics and outputs from our simulations that can help with understanding other interesting inputs and results related to our simulations.

Top 30 borrowers’ aggregate positions & borrow usages

Top 30 borrowers’ entire supply

Top 30 borrowers’ entire borrows

Price changes of key assets since Gauntlet’s last parameter recommendation post on 2022-10-12

Prices for ETH and WBTC have increased, primarily due to upticks in the past few days, thus partly driving a recent decrease in VaR, as shown below.

Time series of Value at Risk (VaR) since our last post on 2022-10-12

Below, Gauntlet analyzes 2 user addresses that are meaningful contributors to Value at Risk per our simulations.

We have been monitoring user 0xe84a061897afc2e7ff5fb7e3686717c528617487, who, as we mentioned in our previous posts, is the main driver behind the occasional high increase in VaR in our daily simulations.

Below are details of the user’s position as of 10/26:

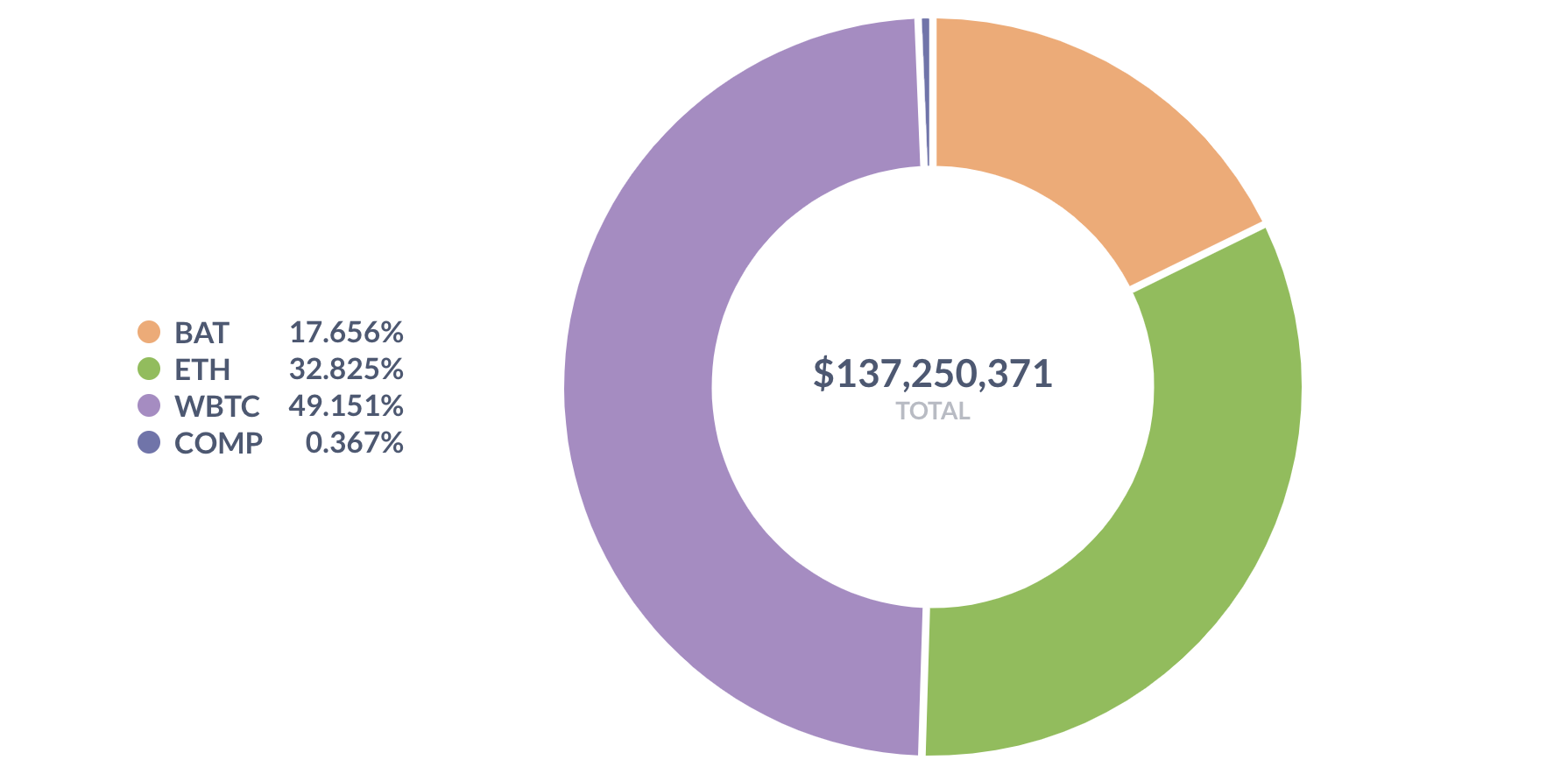

User supply breakdown

Relevant collateral factors

User borrowing power breakdown

User borrows breakdown

User borrow usage

Below is a time series of borrow usage for this user, with the purple bars corresponding to dates when the user actively updated the tokens in their position. From this, we can get a sense of the user’s “intended” borrow usage.

User borrow usage time series since the last post on 2022-10-12

We observe that, as of late, this user has been elastic and intends to have their borrow usage in the low 70%'s.

Note that Gauntlet’s simulations are conservative in the sense that they assume users will not add collateral during a flash market crash, despite observed user elasticity.

In addition, we also occasionally observe SUSHI appear in the VaR figures due to user 0x7e6f6621388047c8a481d963210b514dbd5ea1b9, who accounts for 98% of the total SUSHI supply on Compound.

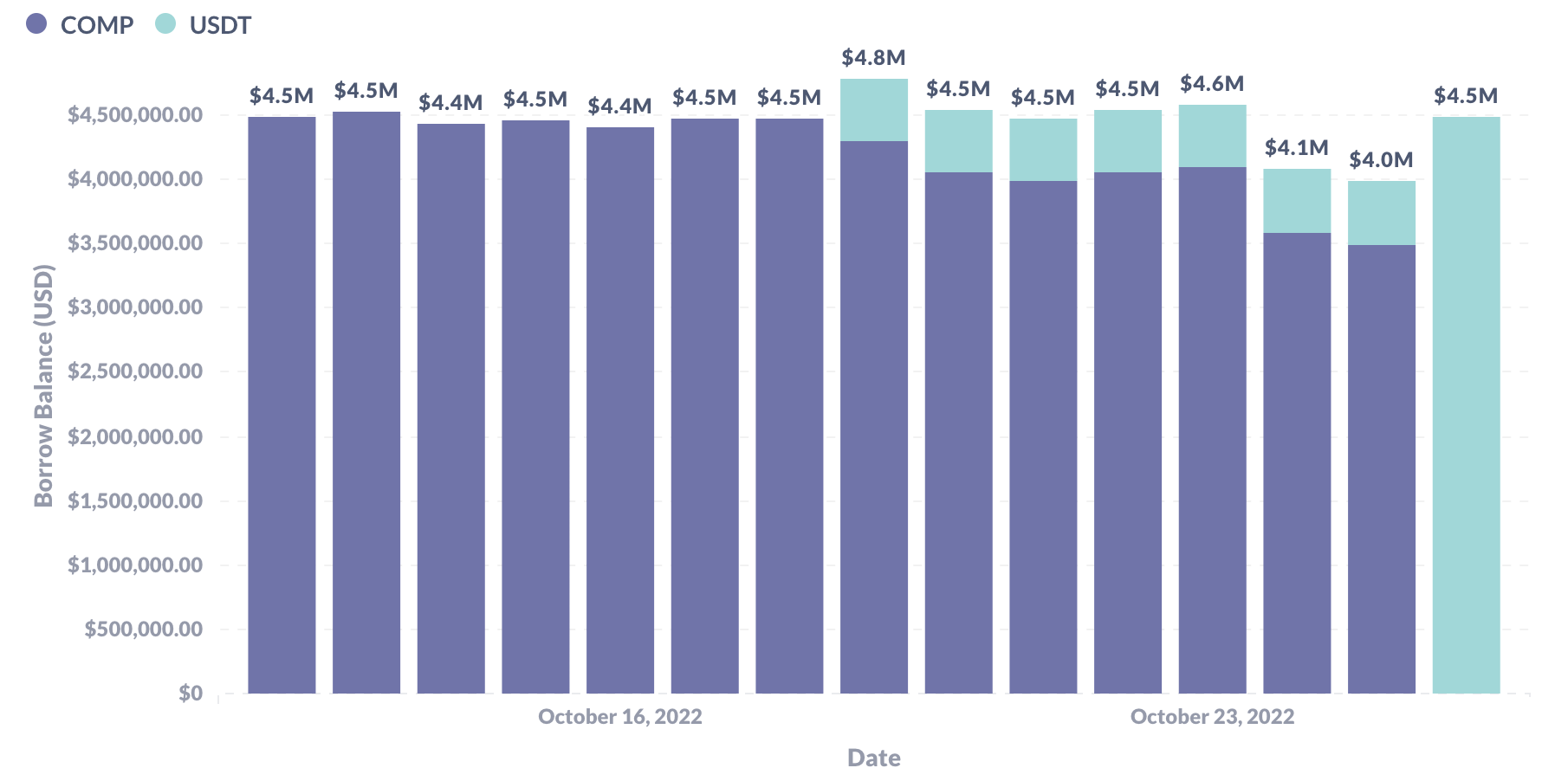

Below are details of the user’s position as of 10/26:

User supply breakdown

Relevant collateral factors

User borrowing power breakdown

User borrows breakdown

User borrow usage

User supply time series since the last post on 2022-10-12

User borrows time series since the last post on 2022-10-12

User borrow usage time series

Note that SUSHI price has increased by 33%, and COMP has decreased by 9% since Gauntlet’s last parameter recommendation post on 2022-10-12. Given this user had large SUSHI supply and COMP borrows, these market changes have given the user substantially more borrowing power. The user responded by updating their supplies and borrows, as seen above, to keep their borrow usage roughly around 70%. Also, in the last day, this user repaid all of their COMP borrows and is now instead solely borrowing USDT.

SUSHI VaR has been high relative to the supply. So, even though this user is elastic, we recommend decreasing SUSHI CF from 73% to 70%, which as of now, will result in their borrow usage increasing from 69.9% to 72.5%. We will continue to run liquidation analyses throughout the proposal to measure whether the CF decrease will result in any risk-off liquidations for this user or any other positions which supply SUSHI.

| Parameter | Current Value | Recommended Value |

|---|---|---|

| SUSHI Collateral Factor | 73% | 70% |

Dashboard

The community should use Gauntlet’s Risk Dashboard to understand better the updated parameter suggestions and general market risk in Compound.

When making recommendations, Gauntlet takes into account the entire distribution of insolvencies and liquidations from our simulations and weighs them against increases in borrows. The below metrics give the community insight into some of the insolvency and liquidation tail risks the protocol could face and Capital Efficiency improvements the protocol stands to gain. Click the collateral-specific pages linked in the Collateral Risk section for more detailed simulation metrics.

Value at Risk represents the 95th percentile insolvency value that occurs from simulations we run over a range of volatilities to approximate a tail event.

Liquidations at Risk represents the 95th percentile liquidation volume that occurs from simulations we run over a range of volatilities to approximate a tail event.

These parameter changes decrease borrow usage by 1 basis point, decrease VaR by $8.15k and decrease SUSHI VaR by 14.3%

Next Steps

While Gauntlet expects to initiate a governance proposal for this set of parameter recommendations on Sunday, 10/30 (voting to begin 2 days later), we will cancel the vote should changes in our daily simulations dictate it necessary.

By approving this proposal, you agree that any services provided by Gauntlet shall be governed by the terms of service available at gauntlet.network/tos.

Quick Links

Analytics Dashboard

Risk Dashboard

Gauntlet Parameter Recommendation Methodology

Gauntlet Model Methodology