Simple Summary

A proposal to adjust one (1) risk parameter for one (1) Compound V3 asset.

Abstract

Gauntlet’s simulation engine has ingested the latest market and liquidity data. These recommendations are Gauntlet’s regular parameter recommendations as part of Dynamic Risk Parameters.

Motivation

In certain market conditions of extreme duress, Compound III’s liquidation mechanism may be subject to holdings of insolvent collaterals. If liquidators can profit from swapping after acquiring collaterals from Compound III at a discount, they will acquire the assets, and the protocol can avoid holding the collaterals over time. Thus, liquidity and liquidation factor are two key exogenous variables for successful liquidations (liquidators call absorb, buying from Compound III and swapping them out). While we cannot directly control the former, increasing liquidation incentives can reduce protocol insolvency risk. Gauntlet’s agent-based simulations use a wide array of varied input data that changes on a daily basis (including but not limited to user positions, asset volatility, asset correlation, asset collateral usage, DEX/CEX liquidity, trading volume, expected market impact of trades, liquidator behavior). Our simulations tease out complex relationships between these inputs that cannot be simply expressed as heuristics.

Analyzing liquidations of the COMP token on the protocol in the last 3 months, approximately 54% (56/103) go through UniV3. However, this number decreases if you only include liquidations of larger size. Namely, the only two liquidations that were larger than 10k: Ethereum Transaction Hash: 0x3a3ba6b0a6... | Etherscan and Ethereum Transaction Hash: 0x3b7296dfee... | Etherscan. Both of these transactions did not atomically sell. Thus, it is necessary to revisit the parameterizations of COMP in the Comet USDC market to better optimize the protocol’s exposure to insolvency risk.

Based on Gauntlet’s simulation results as of 2022-11-30, decreasing COMP liquidation factor from 93% to 88% reduces Value at Risk (VaR) for COMP (showed in blue below) from $5.6m to $4.5m, a ~20% decrease. This reduction is reflected by the increase in the amount of COMP purchased by liquidators in simulation results.

We’d note that VaR here refers to the amount of collateral that has been absorbed by Comet but not purchased by liquidators. In other words, the VaR calculation refers to the value of absorbed collateral that is sitting on Comet’s balance sheet and is subject to pricing risk. This definition of VaR is slightly different from the definition of VaR for Compound V2 in order to align specifically with Comet’s new liquidation mechanism.

We’d also note that given that these parameter changes are for the liquidation incentive, there is not a meaningful impact on capital efficiency.

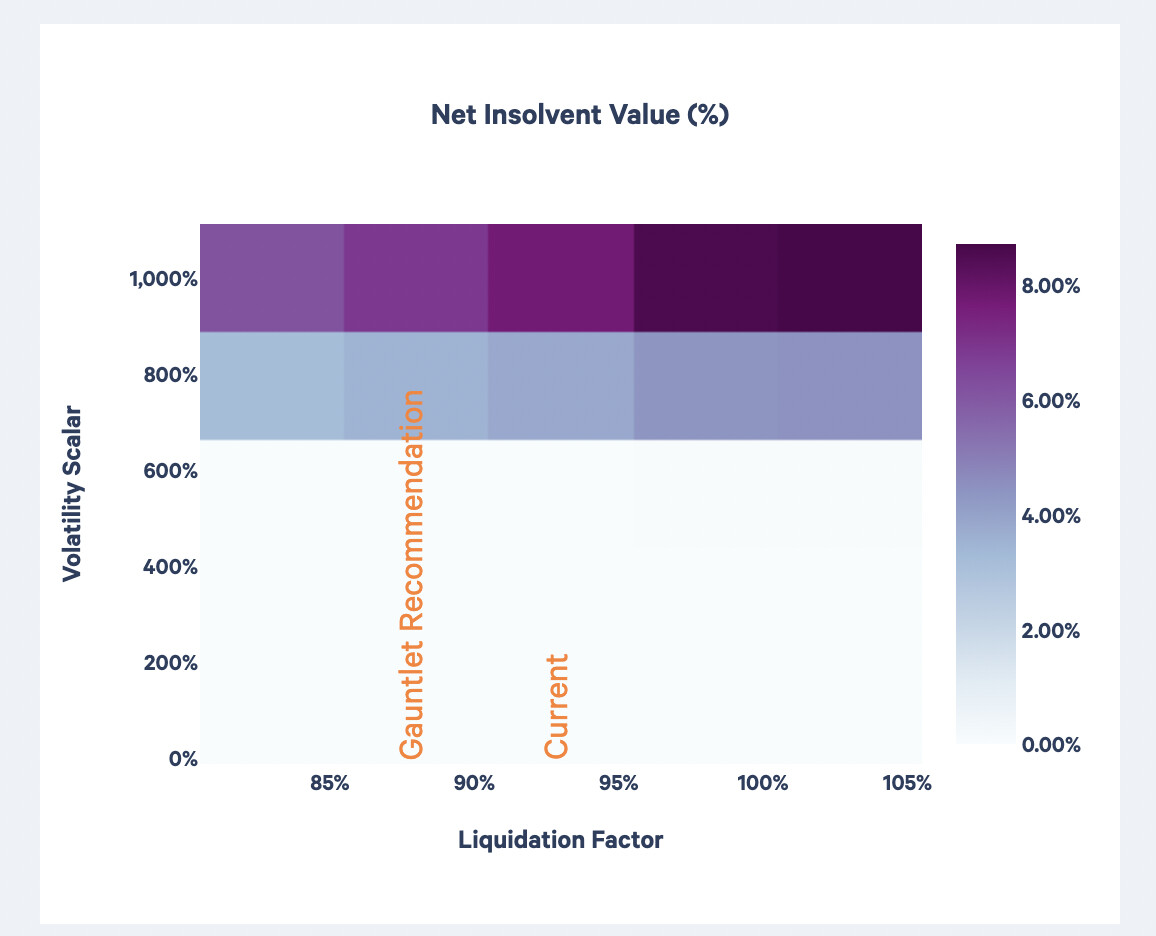

The below heatmap shows the average % net insolvent COMP under different market scenarios. When the market has 10x volatility, decreasing liquidation factor from 93% to 88% drops the insolvency percentage from 7.71% to 6.83%, and when the market has 7.75x volatility, from 3.81% to 3.50%.

Specification

| Parameter | Current Value | Recommended Value |

|---|---|---|

| COMP Liquidation Factor | 93% | 88% |

Next Steps

- Welcome community feedback

By approving this proposal, you agree that any services provided by Gauntlet shall be governed by the terms of service available at gauntlet.network/tos.

Gauntlet launched an insolvency refund for Compound that contains a portion of our payment stream that can be clawed back in the event of insolvencies due to market risk. Since our last recommendation there have been no new insolvencies in Compound. Gauntlet’s Insolvency Refund vault is still live and can be seen here 0x7667095Caa12b79fCa489ff6E2198Ca01fDAe057