A Covered Call strategy is a standard in Corporate Finance. While it can limit the upside of the treasury it’s well known way to continuously generate yield for the Compound DAO. With the recent direction shift of the Morpho Partnership I believe the DAO should generate multiple streams of fee generation. I am happy to support this proposal.

1 Like

I don’t want to make accusations without evidence and I don’t know enough to analyze this. But common sense dictates anyone offering more than 5% return is likely balancing that with risk, and someone that can honestly make 15-35% return yearly safely wouldn’t be asking me for money to do so because they’d be retired on a yacht somewhere. Instagram is filled with ads for 15% returns and we ignore them for a reason. People with no money promising 15-35% returns you should run away from, people with lots of money who can achieve those returns will be doing it themselves not bothering to chase us for money. Common sense to me and I suspect most others dictates we ignore this proposal.

1 Like

Hi @misher and thanks for your feedback. As far as we interpret it, there seems to be a misunderstanding of what an annualized yield means in the context of a covered call.

It is not a constant yield we just generate without any risks or variables, but a different representation of the option premium. Annualizing the option premium is just done to help put it into perspective and make it somewhat comparable to basic yielding products.

For example,

if you use $1.4M worth of COMP (at today’s quotes, we checked hence delay in reply) and write a call with 130% strike and 180-day duration, the upfront premium would be $125,145 = ~8.4% of the notional value of $1.4M worth of COMP, which if annualized is ~16%.

So the annualized yield is basically annualizing the option premium relative to the notional value.

Assuming prices stayed flat, you could repeat again in 180d at same terms, which obviously is a simplification but you get the idea. Hope that helps!

We share a similar view to @Gauntlet with an additional comment on buybacks. The impact of buybacks doesn’t always contribute positively to eco growth - particularly when protocol revenue is invested to purchase tokens at a high market price.

An alternative to a fixed threshold arbitrarily set at $50 (now trading at $39) would be to establish rules based on market dynamics, earnings multiples, and indicators like MA/EMA/VOL—and trigger buybacks when specific ratios fall below a defined threshold.

1 Like

Thanks for engaging with the prop @ExaGroup, we previously responded to Gauntlet’s comments here, and address your buyback comment further down in this post.

Over the past few months we’ve appreciated the thoughtful feedback from delegates, community members, and the ongoing forum discussions. Throughout this process, we have considered all recommendations and made key adjustments to align the strategy more closely with Compound DAO’s priorities.

As a last measure, we’re changing the initial usage and route of the USDC, removing the Enzyme vault out of the equation to instead support liquidity on Compound itself. Resulting cToken positions will be used for cash-secured puts for strategic COMP token buybacks when appropriate. More details below:

Key Updates to the Proposal since V1

Focusing Exclusively on the COMP Covered Call Strategy

In response to Gauntlet’s concern regarding the depletion of working ETH capital, we have removed the ETH strategy from this proposal and are focusing exclusively on the COMP treasury. We propose using a covered call strategy to generate sustainable USDC-denominated yield while maintaining strategic exposure to COMP.

Deploy Converted Stablecoins to Support Compound’s Liquidity

From our discussions so far, we found that the most value-aligned way to deploy stablecoin proceeds is within Compound’s own lending markets to support liquidity supply and foster borrowing activity on COMP.

While funneling stablecoins into external lending markets could potentially generate higher yields, the feedback we received indicates that deploying stables within Compound is strategically more aligned with the protocol’s long-term interests.

Using Yield-Bearing cStablecoins for Strategic Buybacks

Building on feedback from different delegates, we propose using the converted stablecoins from the options strategy to strategically defend the COMP price at key levels through cash-secured puts using Compound-deposited, yield-generating stablecoins, as deemed appropriate pending market conditions.

In other words, if a conversion from the covered call strategy occurs—say, for example, $1 million worth of COMP is sold at a 130% strike price for $1.3 million USDC—we deposit the USDC into Compound. If the COMP price needs to be defended (see the ‘Buyback Triggers’ section below), we use a portion of the yield-bearing Compound USDC as collateral to write cash-secured puts. This allows us to earn additional yield on yield while converting USDC back into COMP if the price falls below the put strike levels, thereby defending and acquiring COMP at favorable prices—eliminating any potential strategic overlap related to USDC accumulation. The bought-back COMP can then be used to rerun the covered call strategy, continuing the yield generation cycle for the Compound DAO.

To optimize execution, we will use technical market signals to help identify and trigger buyback opportunities systematically, see below for further elaboration.

Premium Proceeds to Pay for Delegate Program, Developers, or [insert growth initiative]

The DAO could draw on the USDC premiums and conversion amounts -if any- generated from the covered call strategy to cover ongoing operational costs, such as the delegate program, development work, or whatever it may be.

Execution Plan

1. Deploy COMP for Covered Calls

As outlined previously, we propose using COMP to write out-of-the-money call options that balance maximum upfront premium while keeping conversion probability reasonably low. Since the most recent feedback-based adjustments to the proposal means less focus on depositing USDC into a yield-generating vault and more so on rolling an “options wheel”, we will also adjust the strategy parameters to lower the conversion probability.

- We’ll still target an average 15% annualized option premium, with a +/-5% range caveat in the short term following the lowered conversion probability target.

- Expiry for covered calls will not exceed 180 days.

- If no suitable covered call opportunities meet these parameters, Avantgarde will wait rather than forcing suboptimal trades.

See yesterday’s quotes on a notional amount of $1,480,050, with premiums ranging between 13.2-19.4%:

2. Deploy Stablecoin Proceeds into Compound Lending Markets

- All stablecoin proceeds from option premiums and any COMP conversions will be deposited into Compound lending markets, earning additional yield via Compound-deposited stablecoins cTokens.

3. Cash-Secured Puts for Strategic Buybacks

- We propose continuously monitoring market conditions using technical indicators, as suggested by @ExaGroup.

- If an attractive buyback opportunity is identified, the cTokens will be used as collateral to sell put options on COMP with:

- Strike prices between 80-100% of the spot price.

- Expiries of up to 90 days to optimize for stablecoin liquidity.

Buyback Triggers

Incorporating ExaGroup’s feedback, we propose monitoring key indicators to objectively identify buyback opportunities:

- RSI-Based Trigger: If RSI (14-day) drops below 30, COMP is considered oversold, signaling a potential buyback opportunity.

- Moving Average Crossover (SMA-14 & SMA-50): A buyback signal is confirmed when SMA-14 crosses above SMA-50 after a downtrend.

- MACD Confirmation: If MACD crosses above its signal line, this reconfirms positive momentum and a potential buyback opportunity.

- Market & Earnings Multiples: Additional fundamental market dynamics and earnings multiples can be incorporated to refine buyback execution.

Below is an illustration of historical buyback signals based on these indicators:

Final Remarks

With the refinements outlined above, we believe this proposal strikes the right balance between:

- Activating idle COMP for yield generation.

- Ensuring treasury sustainability.

- Executing strategic, systematic buybacks using yield-bearing cTokens for cash-secured puts.

Given the positive feedback we’ve received from multiple delegates over the last few months, as we have recently stated in this thread, we believe the time is right to move forward with this proposal soon.

As a reminder:

-

Liquidity for writing calls and cash secured puts has been validated; i.e. counterparty interest with institutional trading firms has been confirmed.

-

If successful, the execution of this proposal will be managed through the same multisig structure as the recent Morpho proposal led by Gauntlet; which we hope will be a 3-out-of-5 multisig managed by Avantgarde, Myso, 2 signers from the Compound Governance Working Group, and 1 additional signer to be confirmed.

We look forward to continued engagement with the community and will prepare a Tally governance proposal for consideration shortly and as always welcome any additional feedback to ensure the best possible outcome for Compound DAO.

2 Likes

So the multisig ( within its permissions) can gain that voting power?

Thanks for the question @Gizmoh. The answer is no, there’s no voting power if tokens are not delegated; which they won’t be under this proposal.

We do apologies for the confusion, these advanced treasury controls that you cite are unrelated to the current setup and was shared as an option in v1. Unfortunately, forum settings prevents us from editing the initial post any further. We’ve instead opted for a multisig for the flexibility and fine-tuning in execution that it offers, and to avoid the rigidity and added governance overhead that would both slow down the execution and possibly hurt the performance of the strategy as a result.

The multisig is controlled jointly by Avantgarde, Myso, as well as PGov and Arana from the Compound Governance Working Group, and we’re looking to add a fifth delegate (awaiting answer). This means that if Avantgarde was to try and delegate voting power to itself this would immediately be noticed by the co-signers, who would block any such transaction and inform the community.

Hope that clarifies things!

The proposal is now LIVE on Snapshot: A Growth-Earmarked Treasury Strategy for Compound

See the latest updates and version of the proposal below.

Updates to the Proposal since V1

Based on feedback, a number of changes have been made to the proposal since first draft:

Lowered COMP amount to $1.5m

- Ask lowered from $5m to $1.5m as a first pilot.

Focusing Exclusively on the COMP Covered Call Strategy

- Citing Gauntlet’s concern over working ETH capital, we have removed the ETH strategy and are focusing exclusively on the COMP strategy.

Deploy Converted Stablecoins to Support Compound’s Liquidity

- Using external lending markets may generate higher yields, but the most value-aligned way to deploy stablecoin proceeds is within Compound’s own lending markets to support liquidity supply and foster borrowing activity on COMP.

Using Yield-Bearing cUSDC for Strategic Buybacks

-

Stablecoin proceeds from the options strategy will be used to buyback COMP price at key levels through cash-secured puts using Compound-deposited, yield-generating cUDSC, as deemed appropriate pending market conditions.

-

If a COMP conversion (despite keeping probability reasonably low) occurs from the options strategy, we deposit the USDC into Compound and use the yield-bearing cUSDC as collateral to write put options—earning yield on yield while converting USDC back into COMP at favorable prices—eliminating any potential strategic overlap related to USDC accumulation.

-

To optimize execution, we will use technical market signals to help identify and trigger buyback opportunities systematically, see below for further elaboration.

-

The bought-back COMP can then be used to rerun the covered call strategy, continuing the yield generation cycle for the Compound DAO.

TL;DR

This proposal aims to activate some of the idle COMP in the Compound treasury to improve capital efficiency and boost revenue. The strategy has three parts:

-

COMP Yield Strategy: Use COMP to generate USDC yield. This strategy maintains COMP exposure whilst making opportunistic sales possible at higher prices. In the meantime, it targets to deliver 15% or more annualised net USDC-denominated yield on COMP tokens.

-

Deposit USDC into Compound for cUSDC: Deploy USDC proceeds from the COMP strategy into Compound lending markets, earning additional yield via Compound-deposited cTokens.

-

cUSDC & Yield-Generating Buybacks: Use yield-generating cUSDC as the underlying for put options to earn yield on yield while buying back COMP at favourable key levels.

As each COMP → cUSDC → COMP cycle completes, the strategy can be continuously rolled over to keep generating yield for the DAO.

Outcomes:

-

Earn USDC-denominated yield on COMP (targeting 15% APY).

-

Earn yield on cUSDC proceeds deposited into Compound.

-

Earn yield on yield while buying back COMP at key levels.

-

Enhance capital efficiency and financial sustainability.

-

Stimulate trading volume and market liquidity.

Ask:

- 34k COMP (≈$1.5m as of March 25th) to execute on the outlined strategy to generate USDC for the treasury.

Proposal

This proposal presents a treasury strategy to complement Gauntlet’s reserve management, with the aim of improving capital efficiency and revenue on idle treasury assets to support the DAO’s capacity to fund growth initiatives and improve financial sustainability. The proposed overall strategy includes three parts:

1. COMP Yield Strategy

We propose using COMP to write out-of-the-money call options that balance maximum upfront premium while keeping conversion probability reasonably low. Since the most recent feedback-based adjustments to the proposal means less focus on depositing USDC into a yield-generating vault and more so on rolling an “options wheel”, we will also adjust the strategy parameters to lower the conversion probability.

-

Target an average 15% annualized option premium, +/-5% in the short term following the lowered conversion probability target.

-

Expiry for covered calls will not exceed 180 days.

-

If no suitable covered call opportunities meet these parameters, suboptimal trades will not be forced until the right opportunities arise.

See recent quotes on a notional amount of $1,480,050, with premiums ranging between 13.2-19.4%:

2. Deploy Stablecoin Proceeds into Compound Lending Markets

All USDC proceeds from the option premiums and any COMP conversions will be deposited into Compound lending markets, earning additional yield via Compound-deposited stablecoin cTokens.

3. cUSDC Yield and Strategic Buybacks

Building on feedback from different delegates, we propose using any converted stablecoins from the COMP Yield Strategy to strategically defend the COMP price at key levels through cash-secured puts using Compound-deposited, yield-generating cUSDC, as deemed appropriate pending market conditions.

A cash-secured put strategy involves holding stablecoins while selling a put option on an underlying token (e.g., COMP), think a reverse covered call. Treasuries looking to conduct buybacks can use cash-secured puts at target price levels, committing to repurchasing tokens at a discounted price while earning option premiums along the way.

In other words, if a conversion from the covered call strategy occurs—say, for example, $1 million worth of COMP is sold at a 130% strike price for $1.3 million USDC—we deposit the USDC into Compound. If the COMP price needs to be defended (see the ‘Buyback Triggers’ section below), we use the yield-bearing Compound USDC as collateral to write cash-secured puts. This allows us to earn additional yield on yield while converting USDC back into COMP if the price falls below the put strike levels, thereby defending and acquiring COMP at favorable prices—eliminating any potential strategic overlap related to USDC accumulation. The bought-back COMP can then be used to rerun the covered call strategy, continuing the yield generation cycle for the Compound DAO.

We propose continuously monitoring market conditions using technical indicators (summarised below). If an attractive buyback opportunity is identified, the cTokens will be used as collateral to sell put options on COMP with:

-

Strike prices between 80-100% of the spot price.

-

Expiries of up to 90 days to optimize for stablecoin liquidity.

Buyback Triggers

Incorporating community feedback, we propose monitoring key indicators to objectively identify buyback opportunities:

-

RSI-Based Trigger: If RSI (14-day) drops below 30, COMP is considered oversold, signaling a potential buyback opportunity.

-

Moving Average Crossover (SMA-14 & SMA-50): A buyback signal is confirmed when SMA-14 crosses above SMA-50 after a downtrend.

-

MACD Confirmation: If MACD crosses above its signal line, this reconfirms positive momentum and a potential buyback opportunity.

-

Market & Earnings Multiples: Additional fundamental market dynamics and earnings multiples can be incorporated to refine buyback execution.

Below is an illustration of historical buyback signals based on these indicators:

Implementation and Execution

While the infrastructure setup of the proposed strategy will be fully detailed in a follow up on-chain proposal, this section outlines the implementation from a high level below.

Avantgarde have typically used a combination of Safe multisig roles & permissions (via the Zodiac Roles Modifier) for implementing bespoke treasury management strategies. These setups provide beneficial flexibility to fine-tune execution of the strategy, while still protecting the DAOs assets by setting permissions so that only specific pre-agreed actions on selected protocols can be performed.

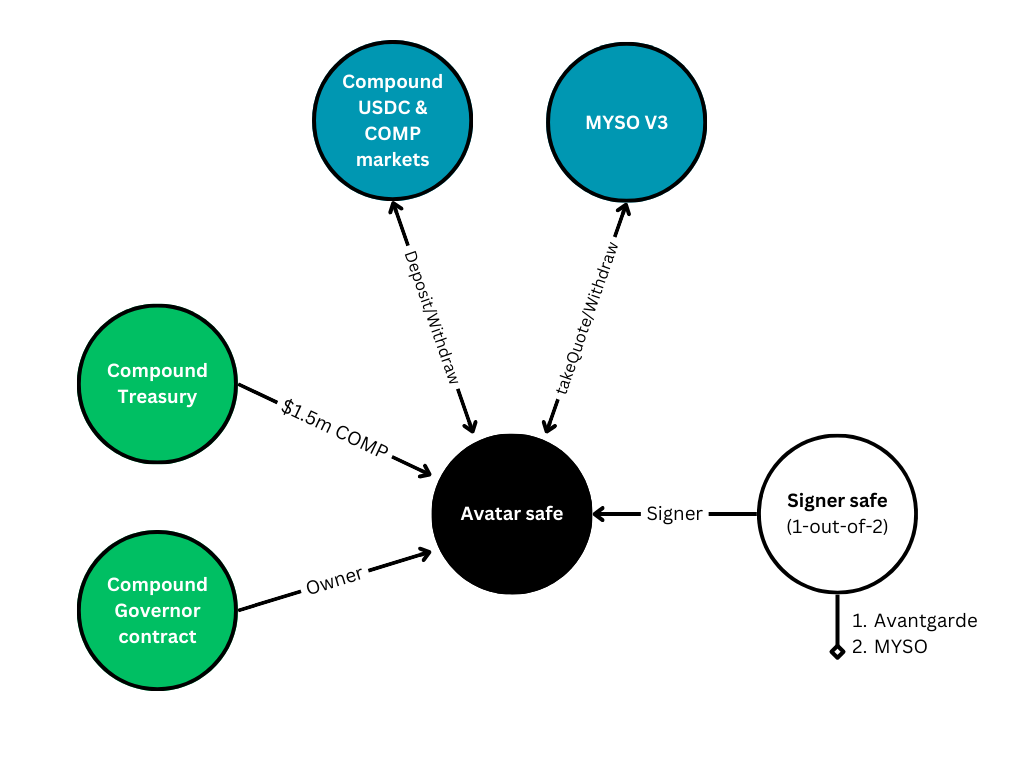

We propose to keep the assets to be managed in a Safe multisig (referred to as the Avatar safe) owned by the Compound Governor contract, and add a separate 1-out-of-2 multisig (the Signer safe) managed by Avantgarde and Myso as a signer on the Avatar safe to execute transactions.

To facilitate efficient trading operations, we will use the Zodiac Roles Modifier to set permissions for the Signers. The value of Zodiac roles is that you can be super granular when it comes to what Signers are allowed to do, to ensure there’s nothing they can do that results in a loss. In this case, the Signer safe will only be able to perform these actions:

-

Depositing in the USDC and COMP compound markets

-

Taking quotes and withdrawing proceeds from MYSO V3 (“takeQuote” and “withdraw” actions on the MysoV3Router contract)

Strategy Execution

Execution of the options strategy will be done through MYSO v3, which eliminates the need for institutional trading firms to take custody of COMP tokens or rely on off-chain legal agreements. The entire process is decentralized, secure, and transparent, ensuring maximum returns while retaining full asset control.

MYSO Protocol Architecture

The protocol consists of two core smart contracts: the Router and the Escrow

Implementation Contract. These contracts are publicly available in the official MYSO V3

repository and have been thoroughly audited (see Omniscia Audit Report). Users only need to interact and approve the core Router contract, which manages all token transfers related to option writing, auction creation, bidding, exercising, borrowing, and fund withdrawals.

When a user writes an option and is matched with a trading firm:

-

A segregated escrow smart contract instance is created, locking the underlying tokens for the option’s duration.

-

The escrow contract mints an option token, which is sent to the trading firm upon match, ensuring atomic execution and eliminating counterparty risk.

-

Upon match, the counterparty must automatically pay the premium to initiate the start. If the limit price is reached at maturity of the loan, the trading firm should pay the agreed strike price; otherwise, the coins automatically unlock after expiry, returning to the Gitcoin treasury, eliminating counterparty risk.

Reporting

-

Quarterly Reports: Detailed written reports on the strategies performance and results.

-

Community Call Updates: Monthly updates to the Compound community.

Compensation

15% on premiums only.

While the proposal is still ongoing, considering the upcoming changes to COMP tokenomics where COMP stakers will be able to gain revenue, would this dramatically change the nature of the proposed Treasury Growth? It would be good to hear the team’s perspective on how it might change or not change the strategy

1 Like

I completely agree, allowing long-term COMP holders to stake and earn could bring an exciting new incentive layer. This could not only make things more engaging for users like myself but also open up new marketing opportunities. For example: offering chains more ways to earn when they integrate or setting up a points-based system, like Sonic, to increase both attraction to compound and TVL.

1 Like

Thanks for raising this question @Doo_StableLab.

The upcoming changes to COMP tokenomics and the potential for COMP holders to earn protocol revenue via staking are indeed a significant development—and one to actively keep an eye on. While the precise mechanics of these changes are still being finalized, we can already say that they would not dramatically change the nature of the proposed Treasury Growth strategy, but rather open the door for complementary enhancements.

Generally speaking, option strategies—particularly covered calls—can be structured around yield-bearing or rebasing tokens. Examples include staked ETH or Compound’s own cUSDC. In these cases, the base yield (e.g. staking yield or lending interest) continues to accrue in parallel with the yield generated from option premiums. This dual-yield structure can offer a compelling and capital-efficient overlay.

If COMP evolves into a revenue-generating or rebasing token through staking, it could be treated similarly. For example, a wrapped COMP token could be created that accrues the staking yield, which could then be used as the basis for option writing strategies. This would allow the DAO to continue earning base yield from staking revenue while layering on additional yield from selling call options.

Alternatively, the revenue generated from staking COMP could also support cash-secured put strategies—using that incoming yield to fund strategic buybacks at attractive levels. This again aligns with the idea of “yield on yield,” reinforcing a compounding effect over time.

In short, the core approach we’re proposing—leveraging idle COMP to earn premium through options while supporting treasury growth—is still highly relevant. These tokenomic changes, once finalized, could actually enhance the strategy’s efficacy and flexibility. We’ll be able to provide a more definitive integration path once the implementation details of staking mechanics are fully clear.

The key takeaway is that we believe option writing strategies and base yield accrual mechanisms are inherently complementary, and we’re committed to adapting and optimizing the strategy in line with Compound’s evolving architecture.

Hope that’s helpful!

1 Like

Gm Comp community - we’re glad to say that the proposal passed with overwhelming support, and want to thank all of you that contributed with feedback and showed your support!

The interest and receptiveness for a native-token strategy of this sort has been very positive, and we’re keen to now showcase the strategy in action for the DAO. We will now ready the infrastructure before we post the proposal to Tally. See below for an outline:

Next steps:

- Set up the Avatar safe.

- Make the Signer safe the manager of the Avatar safe.

- Add permissions using Zodiac Roles Modifier.

- Transfer ownership of Avatar safe to Compound Governor contract.

- Put up a Tally proposal on-chain to move the $1.5m COMP funds into the Avatar safe.

We’ll keep you posted as we progress!

2 Likes

First and foremost, I want to thank @Avantgarde for putting forth this treasury growth proposal for the Compound DAO and for thoughtfully incorporating multiple rounds of community feedback.

Combining a covered call strategy with lending yield and buybacks to create a positive flywheel for the treasury is a creative idea that should be commended.

Platonia committed to delivering quantitative analysis on this opportunity in a recent community call, with a primary focus on the covered call portion of the proposal. I further want to emphasize that any subsequent feedback here is not intended to impede progress at the 11th hour but rather call to attention execution details that will become increasingly important when scaling up the strategy in the future.

The remainder of this post will be structured as follows

- Requests for clarification

- Options execution challenges

- A utility framework for decision making

Requests for clarification

Some of the following technical details may have been left out from the proposal for clarity and accessibility for the broader community. Surfacing them here will be valuable for developing a technical understanding of how the strategy can succeed at scale.

- What was the COMP price used for the indicative quotes given? Alternatively what were the implied volatilities (IVs) quoted? The fairness of the quotes is difficult to assess without one or the other. The remainder of the post uses a COMP price of $40 (roughly the price when the indicative quote was first posted in the forum here) as a reference point which corresponds to an IV of ~160% for the 90d and ~135% for the 180d options.

- How will settlement prices for COMP be determined on MYSO? Are there specific oracles or methodologies the community can review? From MYSO V3’s contracts, it seems like there is an oracle dependency here in the Escrow contract which eventually queries a Chainlink oracle here.

- Are there any more details Avantgarde can provide on the execution timing and sizing of the covered call strategy?

- It’s been stated that there’s confirmed interest from institutional trading firms. Is there a formal agreement in place with market maker(s) on MYSO? If so, what are the parameters of the agreement? Asking since recent indicative quotes for these calls on the MYSO front end show an IV of less than 80% corresponding to a premium of only 0.1% APY.

Generally MYSO’s indicative pricing seems to show low premiums and APYs for deep out of the money calls.

MYSO’s indicative IVs also seem relatively low given the annualized realized volatility of COMP has been around 110% (computed from standard deviation of daily log returns from the past 180 days)

but still far below the IVs of ~160% possibly implied by the indicative quotes from the market maker. - Mind sharing who the market maker(s) are? With only indicative quotes to go on, a customized options trade like this requires a higher degree of trust, so knowing the reputability of the counterparty would be reassuring.

- How will execution quality be measured?

- Are there indicative quotes available for the cUSDC put writing strategy? Will these transactions also take place on MYSO? Asking because the MYSO smart contracts seem to support writing cash-secured puts and they are mentioned here, but unlike for writing covered calls, no indicative quotes seem to be available on the front end.

- Is there historical trade data available on MYSO, especially any transactions on COMP covered calls and cUSDC cash secured puts on COMP or involving the expected counterparties for these trades?

Initial attempts to answer some of these are included below but it would be helpful to get @Avantgarde’s insights as well.

Execution challenges

The benefits of writing covered calls on COMP seem well understood in terms of generating additional yield in exchange for some of the tail upside. There are a lot of potential costs to executing such a strategy which would be good to review.

Review

Option pricing

A theoretical price for European options is given by Black-Scholes which gives the value of a call as where

and

, C is the value of the call, N is the cumulative distribution function of the Normal distribution, S is the spot price, K is the strike price, r is the risk free rate, t is the time to expiry and σ is the annualized volatility of the asset.

When assessing an options quote the implied volatility can be derived from the market price using Black-Scholes. A common phenomenon is that deep out of the money (OTM) options tend to be priced with higher IVs than their at the money (ATM) counterparts. This pattern is often referred to as the volatility smile.

Capital efficiency

While options are viewed as highly capital efficient derivatives in TradFi as they allow for high leverage positions with low margin requirements, they are very capital inefficient in DeFi. In TradFi, this efficiency is underpinned by trust in centralized financial infrastructure, such as the Options Clearing Corporation (OCC), which holds a top-tier credit rating and guarantees the settlement of U.S.-listed options by acting as the counterparty to every trade.

In DeFi, by contrast, trust is not assumed between anonymous participants. As a result, both buyers and sellers typically must lock substantial collateral into escrow contracts, with full collateralization in the case of MYSO V3. Under current designs, the option seller forgoes any yield that could otherwise be earned on the locked assets (e.g. COMP staking). This is likely why on-chain DeFi options have, to date, been sold primarily by retail participants, with market makers mostly on the buy side.

Liquidity

Liquidity is a key consideration of any execution strategy, especially trading illiquid assets. Unfortunately, there does not appear to be a liquid market for COMP options on any open electronic exchange, which likely explains why MYSO was brought in to facilitate direct matching with institutional trading firms.

The most liquid crypto options exchange is Deribit which accounts for ~85% of global open interest. However, the vast majority of this volume is concentrated in BTC and ETH options, with limited markets for other assets like SOL, XRP, BNB, and PAXG. Even for ETH, deep OTM calls on Deribit tend to have very limited liquidity where spreads often exceed 15% and only a few hundred dollars are available at the best bid and offer.

Options market making

Market makers provide continuous buy and sell quotes to ensure liquidity in financial markets, profiting from the bid-ask spread while managing inventory risk. Because providing liquidity is more complex problem than pure arbitrage, options market makers bear all the costs of arbitrageurs as described here in addition to dealing with pricing uncertainty, delta hedging costs, idiosyncratic tail risk and development overhead, some of which will be described in more detail.

Options are highly leveraged instruments, making risk management through hedging essential. The most basic approach is delta hedging, where the spot asset is traded to neutralize the delta of the option position. This can be particularly costly if the underlying asset is illiquid. In COMP’s case, where average daily turnover is only ~900,000 tokens, market makers are heavily constrained in the size of the options positions they can write without incurring substantial inventory risk.

In addition to inventory and hedging constraints, the MYSO auction mechanism itself can introduce additional overhead. While Dutch auctions offer a simple and transparent method for price discovery, they impose a tax on market makers in the form of development time (for modeling and integration) as well as operational attentiveness. For a trader to engage, the auction should roughly be one of the most attractive opportunities in the market over its duration which is not always guaranteed.

Ultimately, all of these costs are priced into a market maker’s quote to ensure profitability, which is reflected in the overall execution cost of the options strategy.

Execution baseline

The proposal mentions targeting a 15% annualized option premium but would benefit from more detail on how execution quality will be evaluated. While the premium received from writing calls is always positive in nominal terms, what ultimately matters is whether that premium is fair relative to the expected value of the options being sold.

As it stands, there is no constraint preventing the sale of deep OTM calls at low prices to meet the premium target while bearing a negative expected return. This is analogous to the impermanent loss Uniswap LPs face impermanent loss who are effectively short volatility. Similarly, writing covered calls realizes losses when the calls are exercised in the money following a price increase.

To evaluate performance meaningfully, premiums should be benchmarked against a fair market value for the options. Realistically, if there is limited retail demand for COMP speculation and the counterparty is consistently a sophisticated trading firm, the strategy is likely to have negative expected value (–EV). That can still be acceptable if the downside is well-understood and reasonably bounded.

Risks

High execution costs

The primary risk to this strategy is simply that the execution costs may prove up too high relative to the premium, driven largely by costs borne from by the market maker, and to a smaller extent, the treasury.

Several factors contribute to elevated costs for the market maker:

- Substantial inventory risk and pricing uncertainty given the absence of a COMP options market on exchange

- High delta hedging costs from greater market impact in an illiquid COMP spot market

- Operational and labor demands in the form of trader attention and dev integration cycles for the Dutch auction and research bandwidth into a pricing model

These costs are likely to be passed on to the treasury through wider spreads or less favorable execution. Since this is a highly bespoke market that doesn’t exist elsewhere, market makers hold significant pricing power and may effectively name their price.

Encouragingly, the indicative quotes received so far appear more favorable than expected, showing a ~200x improvement over MYSO’s quotes in some cases, as seen in the screenshots above. If that pricing holds at execution, it would be a great outcome. However, indicative quotes are by definition non-binding and subject to change, especially at larger trade sizes. Any meaningful deviation from those initial quotes could materially impact the overall execution cost of this strategy.

One way to mitigate this risk is to ensure healthy competition among market makers. Gathering indicative quotes from multiple reputable firms would help demonstrate that the auction will draw real participation. Alternatively, a bilateral agreement could be made with a designated market maker, specifying that the final execution price must fall within a defined range of a pre-agreed pricing model baseline.

It’s important for the treasury to retain any future staking yield from COMP. The simplest approach would be to incorporate this yield into the option premium, though this would require agreement from the buyer. Smart contract solutions exist that could address this (e.g. deliver a Pendle principal token at expiration while the treasury retains the yield token) but these will take time to validate in practice. Moreover, DeFi options volume are still a small fraction of spot and perpetual trading volumes, and there is no real precedent for trading options on staked assets.

Given these constraints, the DAO should anticipate an interim period during which covered call yield excludes staking yield. Both the technical infrastructure and a willing set of counterparties for staked COMP options will need to emerge before such integrations are viable.

The proposal also has 15% of option premiums as compensation which is another contributor to overall execution costs.

Settlement price manipulation

One form of market manipulation involves aggressively trading an asset to influence its settlement price just before expiration. This is sometimes referred to as banging the close. As a hypothetical example, suppose that calls were written on 40k COMP tokens at a strike of $130 and COMP is trading at exactly $130 just before expiration. If the call buyer pushed the price of COMP from $130 to $140 right at the last moment, the calls would finish in the money, allowing the buyer to pocket $400k on options that would have otherwise expired worthless.

To mitigate this kind of manipulation, settlement prices in TradFi are often based on a weighted average price or involve a highly liquid auction like the Nasdaq closing cross. Any oracle used for options settlement should probably adopt similar safeguards to ensure robustness to this type of economic exploit. This risk can also be reduced by staggering options expirations over time, ensuring that no single expiry is large enough to create a profitable manipulation opportunity.

Frontrunning

Another form of price manipulation is frontrunning. If the parameters of a strategy are static, public and therefore predictable, an actor could exploit this to their advantage.

Suppose a call buyer knows that the treasury is targeting a 20% premium on 40k COMP tokens and COMP is trading at $40. At an IV of 165%, this corresponds to writing about 40k OTM calls at a $130 strike with 90 days to expiration (DTE). While there is no COMP options market to frontrun directly, if a buyer knows when an auction will begin, they can move the underlying spot price in their favor.

For example, the buyer could push COMP down to $35 just before the auction. Now, to earn 20% at the same IV, the treasury would need to write 40k OTM calls at roughly a $107 strike with 90 DTE. After the auction, the buyer pushes COMP back to $40 and pockets ~$40k in option value they wouldn’t have otherwise captured. This translates to a 10% annualized loss on capital for the treasury. The larger the trade size, the more profitable this becomes, since the cost to move COMP down is relatively fixed if there’s no change in spot liquidity, while the profit from frontrunning scales with notional size.

This risk can be reduced by executing in smaller chunks and using an average price oracle to determine the spot reference for pricing.

Main takeaway

This strategy has potential, but there are several important risks that need to be managed carefully. In summary:

- Execution costs could be significant. This is a bespoke trade with no active COMP options market on exchange and an illiquid spot market. A lot is riding on the indicative quotes provided, which are around 200x better than MYSO’s. However, these quotes are non-binding, and market makers have considerable pricing power in this context. To reduce the risk of execution costs ballooning, especially at scale, it would be prudent to gather additional indicative quotes or expressions of interest from other reputable market makers and encourage healthy competition. Another approach is to form a bilateral agreement with a designated market maker, using a predetermined pricing model to set clear bounds for acceptable execution.

- Robustness against manipulation is critical. Common economic exploits such as frontrunning and settlement price manipulation could lead to substantial losses for the treasury. These risks can be addressed by executing gradually in smaller chunks over time and using weighted average oracles to determine the spot price input used for auctions and option settlement.

- Metrics for execution quality are essential. Without clear benchmarks, the treasury risks bleeding excessively from execution costs. Tracking effective yield relative to model-based fair value can help ensure the strategy is delivering net positive returns over time.

Utility framework

Just because a strategy is negative expected value (–EV) doesn’t necessarily mean it’s not worth pursuing. Insurance is a classic example: it loses in expectation, but it provides valuable protection against tail risk. Covered calls follow a similar logic, delivering additional yield while only giving up upside in favorable cases where the asset appreciates substantially.

One way to assess whether this tradeoff is worthwhile is by evaluating the strategy through a utility lens rather than purely in terms of expected wealth. This shifts the focus from maximizing average returns to optimizing outcomes in a way that aligns with the DAO’s overall risk preferences and strategic goals.

Overview

Risk aversion

Risk aversion is the willingness to give up some EV in exchange for reduced uncertainty. Most individuals and organizations are risk averse, and the degree of aversion increases with the size of the potential loss. For example, the DAO might easily accept a fair coin flip where heads yields a $50 gain and tails a $50 loss but would almost certainly decline the same flip if it involved $50 million.

This behavior is closely tied to the concept of diminishing marginal utility of wealth where the more wealth one has, the less utility is gained from each additional dollar. As a result, losses tend to feel more painful than equivalent gains feel rewarding.

Utility functions

Risk aversion can be expressed through a utility function, which translates wealth into utility. One canonical example is the isoelastic utility function defined as

This has the property of constant relative risk aversion (CRRA) where

which is to say that risk aversion is determined by the size of the risk relative to wealth.

Another common utility function is the exponential utility function defined as

which exhibits constant absolute risk aversion (CARA) where

so risk aversion is determined by the absolute size of the risk, independent of wealth.

Some possible utility functions for the treasury are plotted below:

Note that the utility values on the y-axis can vary significantly depending on parameterization. The important takeaway is that utility functions allow for relative comparisons e.g. U(A)>U(B) implies that A is preferred over B. However, absolute comparisons like U(A)−U(B) are generally not meaningful on their own.

Applications

Treasury decision making

Utility functions can be a useful tool for guiding treasury management decisions. Instead of having to determine whether an initiative is positive expected value (+EV), it’s more straightforward to assess whether it results in a gain in expected utility (+EU).

Estimating EV typically requires deep quantitative insights about the market, whereas identifying whether a strategy is +EU often comes down to measuring risk and tracking transaction costs. As an example, volatility targeting is probably +EU since it reduces variance with relatively low rebalancing costs.

Some of the rationale for writing covered calls is based on diminishing marginal utility. Losses from these positions generally occur only after wealth has already increased, making them more acceptable. This can be viewed as rearranging wealth changes along the payoff curve to gain utility. In that light, selling upside calls around the point where marginal utility begins to flatten can be a +EU strategy for the treasury.

Strategy stackranking

Utility functions are also helpful for comparing the relative performance of different strategies. For a risk averse DAO, one potentially valuable approach is buying deep OTM puts, sometimes referred to as crash puts. While these cost a premium, they can function like insurance, improving outcomes during sharp downturns. Rearranging wealth from good outcomes to soften the impact of bad ones can be +EU.

Consider the following strategies applied to idle COMP in the treasury:

- Do nothing (idle COMP)

- Writing deep OTM calls on all the idle COMP, targeting a 20% annualized premium

- Writing OTM calls on half of the idle COMP, targeting a 20% annualized premium

- Buy deep OTM puts on all the idle COMP, targeting a 10% annualized premium cost

- Do 2 and 4

- Do 3 and 4

- Write cash secured OTM puts sized for 25% of idle COMP, targeting a 15% annualized premium

To put some numbers to this, assume COMP is trading at $40 and all options have 90 DTE. Below is a table of strike prices that roughly fit the desired option sizing, premium target and strike ranges as IVs change.

| IVs ↓ \ Strategies → | Deep OTM Call | OTM Call | OTM Put | Deep OTM Put |

|---|---|---|---|---|

| 80% | $57 | $47 | $39 | $26 |

| 120% | $80 | $62 | $34 | $20 |

| 160% | $121 | $86 | $29 | $15 |

The chart below shows how utility changes with COMP price moves for each of the strategies, using an isoelastic utility function with γ=1. This corresponds to a logarithmic utility curve, which reflects moderate risk aversion. For this example, IV is fixed at 120% for the instant spot moves.

Some observations:

- Writing puts has the highest utility in the upmoves by a hair, edging out HODLing from collecting the premium. It has by far lowest utility in the downmoves due to the increased long delta over HODLing.

- Crash puts show a more pronounced increase in utility the bigger the price drop, offering strong protection in tail scenarios while only slightly reducing utility across the rest of the curve

- Writing calls further out of the money results in greater utility loss on the extreme upside. This is due to two effects: more contracts are written since the premium per contract is smaller, and these calls appreciate more rapidly as they approach the money. However, the conversion probability to realize losses is much lower

While the above plot provides intuition about how utility changes with instantaneous price moves, those changes in option value may be difficult to realize before expiration due to limited liquidity. A more practical insight comes from analyzing EU at expiration, when option payoffs are fully settled.

To explore this, the COMP price (S) at expiration is simulated using geometric Brownian motion so where

, S0 is the initial price, σ is the annualized volatility and t is the time to expiry.

Each plot below shows how the EU of each strategy varies with σ. Taken together, the set of plots illustrates how this relationship evolves across different levels of IV and risk aversion.

In reading these, note that risk aversion increases from left to right and IV increases from bottom to top.

Some observations

- When realized volatility exceeds implied volatility, crash puts outperform, especially for lower levels of risk aversion where the large gain on the puts overcomes the disutility of the high variance

- When realized volatility is lower than implied volatility, writing covered calls is the best strategy. The gap relative to other strategies widens as IV rises and shrinks with increasing risk aversion

- Lower risk aversion magnifies the difference between OTM calls and deep OTM calls at the extremities of volatility. Deep OTM calls are more favorable when volatility is moderate where they rarely get exercised but still generate meaningful premium.

- As IV decreases, crash puts become more effective in comparison since insurance is cheaper. As risk aversion decreases, EU remains relatively stable or even increases as annualized volatility rises while the performance of other strategies sharply decline.

- Put writing performs worse as both risk aversion and IV increase, where it is largely dominated by writing calls. This is because puts can substantially reduce utility by amplifying losses in the event of large COMP drawdowns. That said, buybacks can offer utility benefits that are more indirectly tied to wealth, such as signaling a value floor and reinforcing confidence within the community, though directly buying COMP on the open market may be more targeted in generating favorable market impact.

Main takeaway

Utility functions provide a framework for the DAO to make more informed decisions and quantitatively assess how different treasury management strategies perform in the context of the DAO’s risk preferences and strategic goals.

The space of potential +EU options strategies is large, with parameterization across strike selection, sizing, duration, option type and combinations thereof. While finding a seller may be difficult, crash puts can offer valuable protection in severe drawdowns. Exploring the possibility of purchasing them outright, or funding them using a portion of the yield from covered calls, may be worthwhile. Also, direct buybacks of spot COMP may be a more effective approach than writing puts, potentially leading to a more significant positive impact on COMP price.

The optimal options strategy can vary significantly with IV and risk aversion. This highlights the importance of the prices the options are executed at and the value of reaching community consensus on the proper degree of risk tolerance.

Hope this was a helpful overview.

Big thanks to @Avantgarde for the work behind this proposal and for bringing MYSO into the fold. Even with some open questions, this seems like a worthwhile experiment for the treasury to start gathering valuable real world data, akin to the Compound Morpho Polygon collaboration.

As with any initiative in DeFi, and especially one involving bespoke option strategies, it is important to remember that good results at small sizes do not necessarily translate at a larger scale. That consideration was one of the main motivations behind this analysis.

There were a number of suggestions included above, which could involve a fair amount of work, so happy to be of assistance—whether that involves joining meetings with market makers to assess indicative quotes or developing a pricing model. Feel free to reach out and also happy to discuss further on the next community call.

1 Like

Thank you for the very detailed feedback and thoughtful questions @victator, glad to hear you deem this to be a worthwhile initiative for the DAO!

Please find our clarifications and comments below, and feel free to reach out or add further comments should you have any remaining questions — we’d be happy to discuss the utility framework further if there’s interest to do so.

It seems there may have been a misconception that the quoted strike prices were absolute. Instead, the strikes are expressed in relative terms—e.g., 130% or 150% refers to 1.3x or 1.5x the spot price at the time of quote generation. This is common in options markets to account for the dynamic nature of spot prices and facilitate comparison across time.

The indicative quotes referenced were validated on March 10. At that time, the reference spot price was $42.90. Thus, the 130% and 150% strikes correspond to absolute strike prices of $55.77 and $64.35, respectively.

Assuming a risk-free rate of 5%, the implied volatilities were approximately:

-

90-day tenor: 130% strike – 66.4%, 150% strike – 74.2%

-

180-day tenor: 130% strike – 60.3%, 150% strike – 67.4%

As mentioned above, strikes and premiums are quoted in relative terms and then settled using the spot reference at the time of execution. In the simplest case, this is handled manually—by collecting firm quotes from trading desks, selecting the most competitive one, and executing with a reference price at the time of trade.

Here’s an example of such a tradeable quote for another instrument (requires you to connect to Ethereum):

In this model, an oracle is not required, as the absolute strike and premium are locked in at the time of trade creation and validated by signature. The DAO, respectively, the execution multisig has a set time window (typically 15–30 minutes) to execute the trade.

Alternatively, a Dutch auction mechanism can be used. In that case, an external oracle feed for COMP would be used to convert relative strike and premium terms into absolute values at initiation.

Yes, there is confirmed interest, as we have received tradeable quotes—that is, quotes that could have been executed at the time (though they are now outdated, so refreshed quotes would be required at the time of trade). Re indicative quotes on frontend: Again, it’s worth reiterating that strike prices are quoted in relative, not absolute terms. Comparing the quotes against an assumed absolute strike (e.g., $130) can lead to misinterpretation. The indicative quotes shared were from a month ago, and both spot prices and institutional IV pricing evolve over time—hence the associated premiums will vary accordingly.

It’s also important to differentiate between realized volatility, which is backward-looking, and implied volatility, which reflects forward expectations and embeds a margin for model risk and compensation. For example, ETH 79-day ATM implied volatility was recently ~69%, while realized volatility over the same lookback was ~80%. This discrepancy is common and reflects standard market dynamics.

As a guideline, we suggest defining a minimum target annualized yield for a given relative strike. If the premium offered doesn’t exceed that threshold, no trade would be executed.

We work with reputable institutional trading firms such as STS and GSR, among others. If the Compound DAO or Platonia has preferences for specific counterparties, we’re happy to explore those relationships—chances are we’re already in touch.

Importantly, since these trades settle on-chain, the DAO is not exposed to counterparty risk. COMP tokens remain in escrow until execution, unlike traditional OTC flows where assets are transferred off-chain.

Execution quality will primarily be assessed based on quote competitiveness—specifically, how closely aligned the premium offers from different trading firms are for a given strike and tenor. The smaller the spread between quotes, the stronger the indication of a fair and efficient market. In addition, we monitor the consistency of implied volatilities quoted across similar instruments and maturities. Should the DAO wish to define specific execution benchmarks we are happy to integrate those into the quote selection and validation process.

Yes, for example, $1M notional cash secured put on COMP with 90d to expiry and 90% strike (meaning COMP price would have to fall by at least -10% for put to expiry ITM) the option premium as of 8 April 2025 would be at least $26,055. These transactions can also be settled via MYSO’s on-chain infrastructure.

There is no historical trade data for COMP-related strategies yet as Compound hasn’t used MYSO so far.

On Execution Challenges

Capital Efficiency

The concern about capital inefficiency may stem from a misunderstanding. In this case, the DAO treasury already holds the COMP tokens that would be locked into escrow for the covered call. There is no additional capital outlay or margin required. The premium is paid upfront by the trading firm. And since the COMP remains in a smart contract until expiry, there is no counterparty risk.

If and when COMP staking becomes live, we could explore integrating staking yield with covered call strategies—similar to how liquid staking tokens (LSTs) are already supported on MYSO.

Liquidity

As stated earlier, institutional interest in trading these structures has already been validated. While Deribit is the primary exchange for BTC and ETH options, other assets (like COMP) are typically traded OTC—consistent with how non-standard options are handled in TradFi. Thus, the absence of exchange-based liquidity for COMP is not unusual and does not preclude active OTC trading.

Options Market Making

We agree that trading firms must price in their cost structures, including delta hedging, development overhead, and inventory risk. We appreciate this being explained.

Execution Baseline

One could set a baseline for acceptable trades, including strike and expiry combinations the DAO is comfortable with, as well as a minimum annualized premium target. Importantly, the better the quote we source, the higher our absolute fee—so our incentives are fully aligned with the DAO’s.

Settlement Price Manipulation

The risk described seems somewhat mischaracterized. In physical settlement, the trading firm pays stablecoins to the DAO in exchange for COMP held in escrow. There is no need for an oracle at settlement and hence the manipulation scenario described is not applicable.

Frontrunning

Since Avantgarde facilitates the trade matching and auction processes, and firms do not know in advance whether their quote will win, frontrunning is not a viable risk vector here.

On the Utility Framework

We found this framework and the utility-based approach very insightful. If the DAO finds it helpful, we’d be interested in collaborating further with @platonia to refine it. This type of lens could be instrumental in developing principled risk-adjusted strategies.

2 Likes

Gm Compound community - First off we’d like to thank @jbass-oz and the OpenZeppelin team for reviewing the proposal and giving us the green light.

The proposal has been queued on Tally and will be going live in a few hours: Tally | Compound | A Growth-Earmarked Treasury Strategy for Compound

We appreciate all the support we’ve received from delegates on the Snapshot temp check, and look forward to start executing this strategy for the DAO!

1 Like

Proposal 432 Review

OpenZeppelin reviewed Proposal 432 and confirms it is consistent with the draft proposal reviewed previously. We expect the proposal will execute as intended if enacted and will transfer COMP to a multisig configured to constrain operations to only those necessary to execute the proposed strategy. The report is available for the community to review.

1 Like

Hi @Avantgarde, thank you for the detailed response and for providing helpful clarifications. Congratulations on the successful proposal, excited to see the strategy in action!

Apologies for the delayed reply, the vote was a good reminder so wanted to share some follow-up questions and comments while they’re still top of mind. As with the previous post, the intent is to highlight execution details that will be important for future scaling.

Will respond inline first in detail and then provide a brief overall summary and general feedback along with some suggestions at the end.

Inline Feedback

Thank you for the clarification on quoting strikes in % not in absolute terms. The reference used was the indicative quote you posted

Regardless, this doesn’t affect the directionality of any of the points made in my previous post, as incorporating the updated numbers leads to the same takeaways.

Crypto options are still a very nascent market, so the common vernacular around quoting is still developing. That said, the vast majority of electronic options are quoted using an explicit strike price, not just a relative strike percentage, with some exceptions, like exotic instruments (e.g. barrier options) where the payout depends on relative levels. The main reason is simple: for a quote to be tradable, both parties need a spot reference price they agree on.

The dynamic nature of spot prices actually makes it more informative to share both the spot price and the strike price, rather than just the strike as a percentage of spot. This provides better context for comparing quotes over time. If the spot price moves significantly, the volatility surface will shift and the quotes could change substantially. With only the relative strike percentage and time to expiry, two quotes with the same parameters received moments apart could differ dramatically, which is hard to interpret without knowing the spot price.

For these reasons, it is preferable to provide both the absolute spot and strike prices, along with the time the quote was received.

Thank you for providing the reference spot price. Including the time of day the quotes were received would also be helpful, given the dynamic nature of spot prices as you noted. Based on the provided numbers, it appears the quotes were received around 17:00 UTC, when ETH was trading near $2000. Below is a comparison of ETH call IVs at comparable relative strikes and maturities on Deribit against the indicative COMP quotes:

| Quote ↓ \ Calls → | 130% 90DTE | 150% 90DTE | 130% 180DTE | 150% 180DTE |

|---|---|---|---|---|

| COMP (indicative) | 66.4 | 74.2 | 60.3 | 67.4 |

| ETH (Deribit) | 67.7 | 69.6 | 68.6 | 69.8 |

Notably, the indicative COMP quotes are priced less favorably than analogous ETH options, despite COMP being a substantially more volatile asset. For context, here is a plot of 90 day realized volatility (RV) for BTC, ETH, and COMP since the start of 2024:

As a crude benchmark, theoretical COMP IVs can be estimated by scaling ETH IVs using the realized volatility (RV) ratio between COMP and ETH. While this approach is admittedly simplistic, it serves as a useful reference point, and it is always prudent to “trust but verify” rather than rely solely on market maker quotes without independent checks.

On March 10, the RV ratio was approximately 1.4. Assuming a 5% risk-free rate and applying the Black-Scholes model gives the following pricing comparison:

| 130% 90DTE | 150% 90DTE | 130% 180DTE | 150% 180DTE | |

|---|---|---|---|---|

| COMP (indicative) | $2.06 | $1.39 | $3.63 | $2.88 |

| COMP (theoretical) | $4.24 | $2.91 | $7.84 | $6.25 |

| Slippage | 51.5% | 52.2% | 53.7% | 53.9% |

Of course, the theoretical premiums here do not account for market maker costs, whereas the indicative quotes do. However, given the challenges of pricing COMP options without an reference market on exchange and the tight concentration of slippage across quotes, it’s plausible that market makers used a similarly basic approximation model and applied an across-the-board 50% markdown, setting prices to target a 100% return on capital.

Given this, it’s worth asking whether these are truly the most competitive prices available from market makers. If this is indeed the best pricing that can be sourced, the DAO should carefully reconsider whether pursuing these trades is justified, especially when compared to alternatives such as TWAPing spot COMP at higher price targets.

The question behind the question here is how the reference spot price used for the trade is determined. Typically, this is done via an oracle, but if no oracle is used, how is the execution quality of a quote evaluated relative to the absolute strike? How is the absolute strike even determined in the first place? From our discussion so far, would have imagined a reference price is established first and then scaled by 30%, 50% etc to set the strike.

The key point is that some form of reference pricing should be used, as not using one effectively amounts to blindly trusting market makers. Regardless of the method chosen, many of the same attack vectors used to manipulate oracles are likely still relevant. In general, deviations between the reference spot price and the fair market price will tend to increase execution costs.

This time window could add to market maker costs since it gives the DAO a free option to back out of the trade if the spot price moves unfavorably within this interval. Making this window smaller could help reduce execution costs.

Is there a specific COMP oracle address for the Dutch auction @Avantgarde could share for the community to review?

The spirit of my question was to highlight that this strategy may carry significant execution costs.. Gradually executing over time and in smaller sizes can help mitigate these costs. The response provided did not address this question. Would @Avantgarde be willing to share more details on this aspect?

Kindly address these questions as they were not covered in the previous response.

I’m aware of the difference ![]()

The example of ETH ATM IV vs RV provided is an anomaly since IV is generally higher than RV, a relationship that has been extensively researched. A strong contributing factor behind this difference is the presence of the volatility risk premium which has been well documented in financial markets, including decades of empirical observations in the S&P 500.

During periods of extreme market stress, such as the 2008 GFC, Covid, or the recent tariff shocks, RV can temporarily exceed IV if markets have underpriced the magnitude of price swings. Since RV is backward-looking and IV is forward-looking, IV often declines more quickly as a shock subsides, while RV remains elevated because it still incorporates recent large moves within its calculation window. We’re currently in such a period, but under normal market conditions, RV is generally lower than IV, which is why it serves as a useful and conservative input when assessing execution pricing.

Below is a plot of ETH RV compared with IVs ATM and at 130% and 150% call strikes since the start of 2024:

As shown in the chart, the volatility smile is evident, with deeper OTM calls exhibiting higher IVs. In the context of this trade, it is the IV at the specific OTM strikes being traded that matters, not the ATM IV, which further underscores that RV typically serves as a conservative lower bound when estimating fair pricing for options.

With that in mind, the COMP RV plotted earlier offers a rough indication of the IV levels that can be considered broadly fair, which is why they were referenced initially.

This guideline seems insufficient for the treasury’s needs. The proposed annualized yield measure only considers the premium received and does not account for execution costs arising from the gap between fair value and execution price.

Moreover, setting a premium target solely based on relative strikes ignores potential shifts in the forward volatility curve. Even if the DAO sets a seemingly reasonable annualized yield target upfront of around 15 percent, no trades would occur if IVs fall sharply, as the yield would be too low. Conversely, if IVs spike, the treasury risks selling volatility far too cheaply, especially given that no clear framework for monitoring execution costs has been presented so far.

At the very least, a reasonable slippage target should be set, and preferably a utility framework is applied to ensure the trade remains +EU after accounting for execution costs. Ideally, the trade is roughly the most +EU compared to alternatives, such as covered calls at other strikes and maturities or spot strategies like sales at price targets and buybacks.

Kindly address this directly. While the example mentions deep OTM calls, the core concern applies to any option, and the underlying issue remains the same.

Thanks for sharing these details, and it’s reassuring to hear that established market makers are involved. The spirit of the question was less about counterparty risk and more about the concern that the quotes provided may be unfavorable relative to fair value, and that indicative pricing is subject to change. As the trade is currently structured, the execution costs seem high. Happy to assist in negotiating with trading firms if helpful (have talked with firms such as QCP in the past).

This raises some concerns. In an opaque OTC market without an exchange-traded reference price, market makers effectively set their own prices.

Importantly, tight spreads between quotes do not necessarily indicate a fair or efficient market. They can also reflect implicit coordination among participants seeking to maximize their profit from the DAO. For example, if all quotes cluster within 1 percent of a 100 percent markup over fair value, this does not reflect competitive pricing, especially if the DAO lacks a clear framework for assessing fair value and identifying when it is overpaying.

It is also critical to distinguish between receiving one quote (monopoly), two quotes (duopoly), five quotes (oligopoly), and operating in an open electronic exchange (competitive market). Each has vastly different implications for market fairness and efficiency. The fewer counterparties involved, the greater the need to carefully assess execution quality.

Using a reference price of $37 for COMP on that date and a risk free rate of 5% a premium of $26,055 corresponds to an IV of just ~36%. By comparison, the corresponding 90% strike 90DTE ETH call on Deribit at the same time was trading at an IV of ~69%. Using the same model approximation as before of backing out a COMP IV by scaling the ETH IV by the RV ratio (~1.85 on that day) leads to an IV of ~128% or a premium of about ~$184,000. While it’s unrealistic to expect to transact at fair price, the indicative floor given is more than 600% off from estimated fair.

While the premium quoted was intended to be a minimum, would hope the floor is set meaningfully higher and more aligned with estimated fair value.

Could @Avantgarde point to the specific part of the following section referenced that they feel is incorrect or reflects a misunderstanding?

The core point being made here is that TradFi options exchanges generally do not require you to post anything close to 100 percent collateral upfront in escrow. The DeFi design is materially more capital inefficient than its TradFi counterpart.

For example, on the NSE (National Stock Exchange of India) which ranks as the largest options market in the world by some measures such as notional turnover and is entirely physically settled, the delivery margins only begin at 10% on T-4 (4 days before expiration) and ramp up to 70% by T-1.

Idle COMP, by contrast, can be deployed to earn yield in many ways, including liquidity provision, lending, converting into stablecoins or major assets for staking or to use as collateral to short COMP on perpetuals exchanges such as Hyperliquid and collect funding rates in a delta-neutral manner for the treasury. None of these opportunities are available when COMP is locked in escrow so there is inherent opportunity cost, which warrants acknowledgment from @Avantgarde.

It is also important to highlight that locking yield-bearing tokens like stCOMP or cUSDC in escrow is not equivalent to TradFi capital efficiency. If the option is exercised, all the yield accrues to the buyer, which is very different from a system where the seller only needs to deliver assets a few days before settlement and retains nearly all the yield earned prior to delivery.

Put simply, if the seller only needs to post assets shortly before expiry, only a few basis points of opportunity cost are foregone compared to percentage points lost from locking funds away for 90 to 180 days in escrow under the current design.

COMP spot is illiquid. COMP options not having any open exchange market makes them extremely illiquid and their trading highly opaque.

By no means is this a good thing, especially since a COMP trade has never been done before on MYSO.

Regarding the mention of active OTC trading in COMP options, how do we “trust but verify” when no publicly available data exists?

Would expect high execution costs for COMP spot and much higher for COMP options. Happy to be pleasantly surprised by what can be sourced.

This does not mean the trade should be dismissed, but it does suggest the DAO should proceed with caution and remain highly mindful of execution costs. Ultimately, the objective here is not to establish an active OTC market or execute the trade under any terms, but to ensure the DAO secures fair and efficient pricing.

@Avantgarde is a longstanding and respected member of the community, and their contributions to the DAO here should not be understated. That said, the current arrangement leans more toward a trust-based model rather than offering full incentive alignment without potential conflicts of interest.

Respectfully disagree with the claim that incentives here are fully aligned. An analogy is a realtor selling your home. Even with the best intentions and a strong professional reputation, the realtor’s commission creates an inherent incentive to close the deal, even if that sometimes means accepting a lower price, because the realtor is still compensated while the homeowner bears the financial impact. Similarly, commission-based compensation here does not by itself ensure that the DAO’s goals of minimizing execution costs and maximizing treasury growth are fully upheld.

At its core, this dynamic reflects a classic principal-agent problem, where the DAO as principal seeks to maximize execution quality and treasury outcomes, while the agent (in this case @Avantgarde) has compensation tied to trade volume rather than pure outperformance, creating the potential for incentive misalignment even when acting in good faith.

The fundamental conflict arises when market maker quotes fall meaningfully below fair value. If the DAO declines the quote, @Avantgarde does not receive a fee. If the DAO accepts the quote, @Avantgarde is compensated while the DAO absorbs the cost.

There is clear partial alignment when @Avantgarde pushes for better terms, for example, raising a quoted IV from 60 to 70, which increases the DAO’s premium and fairly warrants compensation. However, if fair IV is 100 and the trade clears at 70, the DAO bears a significant execution cost, and the incentives begin to diverge. In that case, the DAO’s loss becomes revenue for @Avantgarde and profit for the market maker. If quotes consistently come in 20 percent below fair value, the DAO effectively takes a 20 percent mark-to-market loss while @Avantgarde and primarily the market maker benefit.

Expect this trade may well be negative EV for the DAO. While that may be tolerable within the DAO’s utility framework, it underscores why strong accountability on execution quality is essential.

In traditional finance, fund managers are held to well-established accountability standards. These include prospectus disclosures, audited financial statements, regulatory filings, index tracking, and public reporting of tracking error. Investors can easily assess whether a fund is meeting its objectives or underperforming relative to its benchmark,

For example, QYLD, an $8 billion AUM fund that sells covered calls on the Nasdaq 100, serves as a useful analogue for the proposed COMP covered call strategy. QYLD tracks the Cboe Nasdaq-100 BuyWrite V2 Index and its fact sheet and historical reports shown below disclose annual returns and tracking error, providing investors a clear picture of performance against its benchmark.

Without comparable accountability measures, the DAO risks operating in a highly opaque environment where neither market makers nor facilitators are reliably evaluated on execution quality. Simply stating that incentives are aligned because fees scale with trade size misses this fundamental risk.

Spreading execution over time and in smaller tranches is also a sensible, practical step that reduces slippage and improves outcomes, even if it lowers market maker profits and intermediary fees.

A constructive path forward would be to define a clear benchmark index, track performance against that benchmark, and measure tracking error. Incentive compensation could then be tied to outperformance of a reasonable execution cost relative to the benchmark, with reduced compensation if underperformance exceeds an agreed upon threshold.

Agree that since this is physically settled instead of cash settled the specific manipulation scenario described is not applicable.

This is great! Let’s celebrate having fewer risks ![]()

Would @Avantgarde be willing to share more details on the specific mechanisms used to prevent frontrunning by “facilitating the trade matching and auction process”?

As mentioned earlier, the Dutch auction relies on an oracle:

If this oracle is a standard Chainlink oracle and there is foreknowledge of when the auction will start, the frontrunning attack previously outlined is feasible.

As requested earlier, it would be helpful to provide the implementation logic of the external oracle feed or offer explicit robustness countermeasures if using a standard Chainlink oracle. This consideration also applies more broadly to any reference spot price mechanism for quoting, auctions and general trade execution.

To address your point more directly, the fact that firms do not know in advance whether their quote will win, while helpful, is unfortunately not a sufficient deterrent to this type of attack. If the auction starts quoting at a price that is too low, all buyers stands to benefit in expectation. Whether or not they know they will win affects only the scale of the opportunity, not the fundamental incentive to push the price down.

These dynamics are common to RFQs in traditional finance. While no participant knows in advance whether they will win an RFQ, the mere signal of intent to trade can influence the market. A prominent reason is that market makers often need to hedge their potential exposures.

For example, generating a 15% annualized premium on 1.5M through 130% strike 180DTE COMP calls with an estimated IV of 120% requires writing about 10.5k calls. Each call has a delta of ~0.55 so delta hedging requires selling 5.8k COMP which is ~65 bps of the average daily volume. Even during this initial experiment phase, there is likely going to be substantial market impact from market makers selling spot in anticipation of the covered call trade, and this will become much more pronounced as the strategy scales.