As outlined in our earlier forum post, [Gauntlet] Compound Market Downturn Analysis (2024-08-05, Gauntlet has conducted further analysis on the liquidation performance within Compound v3. This report aims to provide a detailed breakdown of the liquidation mechanism. Additionally, it examines the impact of delays in acquiring collateral reserves and their effect on liquidation efficiency and protocol stability. The analysis culminates in recommendations for the community to enhance the liquidation performance and address the risks identified during market downturns.

Brief Overview of Liquidations

As detailed in the Compound liquidation documentation and our prior analysis of the liquidation mechanism, Compound v3 employs an absorption mechanism in which the entire collateral is taken over by the protocol, which then settles the user’s debt. The absorbed collateral is then put up for sale, with a sale price determined by the LP and the Store Front Price Factor. Liquidators would purchased the discount collateral to repay the base tokens that settled the user’s debt, plus earn reserves for the protocol. Here is a detailed breakdown of each step:

1. Liquidation Eligibility

An account becomes eligible for liquidation when its borrow balance exceeds the thresholds defined by the liquidation collateral factors. This threshold ensures that the collateral provided is sufficient to cover the debt amount.

2. Absorption Mechanism

A liquidator, which could be a bot, a smart contract, or an individual user, can initiate the liquidation process by invoking the absorb function. This function performs the following actions:

- Collateral Transfer: The

absorbfunction transfers ownership of the collateral from the undercollateralized account to the protocol. - Value Adjustment: The value of the collateral is calculated, and a penalty—referred to as the

liquidationFactor—is subtracted. This factor represents a percentage deduction from the collateral’s value.

The debt on the liquidated account is removed, and the liquidated user is left with a base asset minus penalty.

3. Protocol Reserves and Collateral Management

Each absorption is financed by the protocol’s base asset reserves. In exchange, the protocol acquires the collateral assets. If the remaining reserves fall below a governance-defined target, liquidators are permitted to buy the collateral at a discount using the base asset. This transaction enhances the protocol’s base asset reserves.

4. Seized Collateral Sale and Ask Price

To facilitate the repayment of absorbed account borrowings, the protocol must liquidate the seized collateral. The Ask Price—which determines the discount price of the asset—functions as follows:

- The

Ask Priceis determined by the protocol’s price feed and configured by governance. It is derived from theStoreFrontPriceFactorand the asset’sLiquidationFactorusing the formula:

Delay Purchase of Reserve Collateral

As mentioned in our Market Downturn analysis, significant delays were observed in the absorption and subsequent purchase of collateral. Specifically, within the BASE USDC Comet, WETH collateral reserves exhibited an outstanding delay of 40 hours between absorption and purchase. Similarly, the OP USDT Comets experienced a delay of 7 hours, while the OP USDC Comets faced a 4 hour gap between the absorption of collateral and its purchase. These delays highlight unhealthy liquidator ecosystem, which can impact the Comet liquidity and incur insolvencies to the protocol.

BASE USDC Comets

Optimism USDC/USDT Comets

Reviewing the BASE slippage for WETH collateral during periods of market stress, it was observed that despite a decrease in overall liquidity, decentralized exchange (DEX) liquidity remained adequate to support liquidations. Specifically, $250,000 worth of WETH could be liquidated at a slippage rate of 1% during the downturn. This indicates that there was sufficient liquidity in the market for this blue-chip asset, enabling liquidators to execute profitable liquidations despite the market’s volatility.

Despite the observed delays in purchasing collateral not adversely affecting Comet reserves—indeed, resulting in higher reserves—the potential implications of such delays could be severe under different market scenarios. If these delays had resulted in significant losses, the protocol could have faced substantial risks.

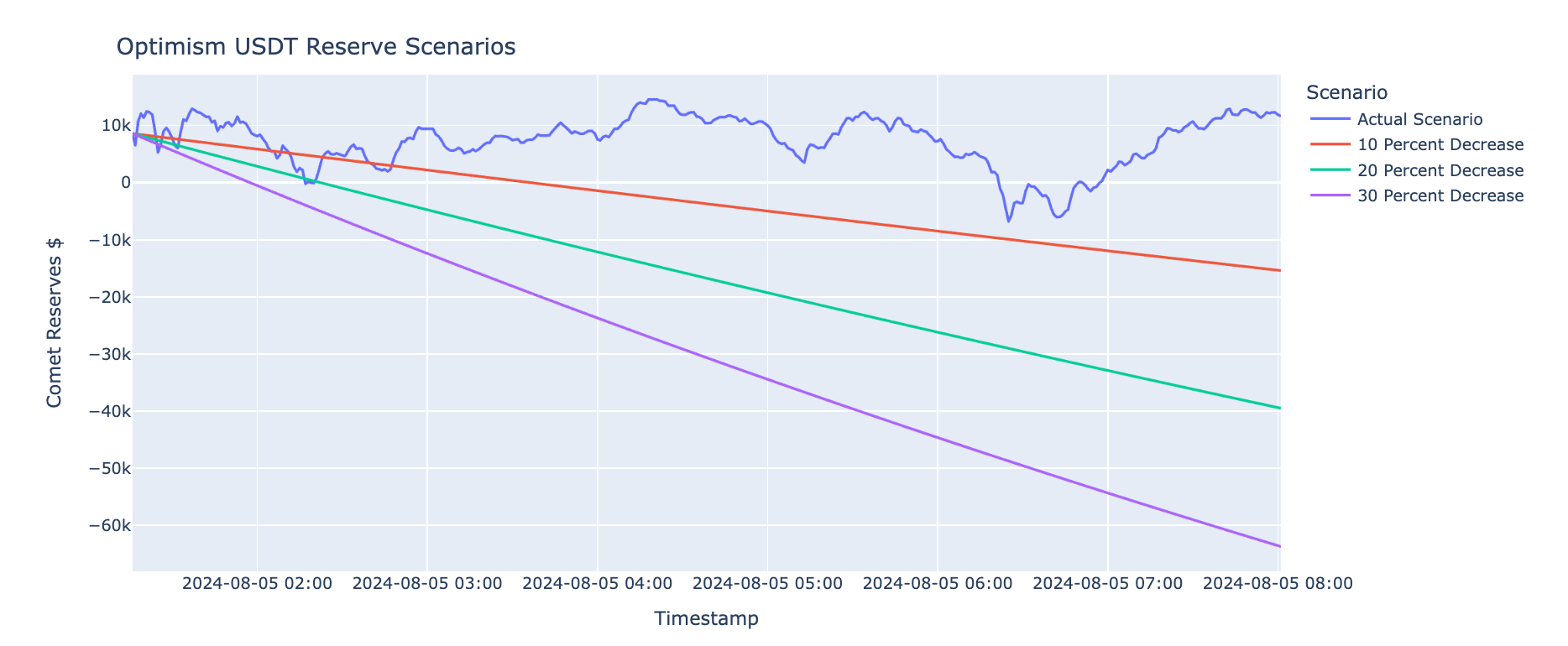

To illustrate the potential risk associated with the delayed liquidation of absorbed collateral, we have developed hypothetical scenarios to assess the impact of a similar 7-hour delay on the OP USDC Comet. These scenarios provide insight into the possible detrimental effects and financial implications of such delays in collateral purchases post-absorption.

This scenario presents the net reserves for the Actual outcome and various price drop conditions. Notably, the reserves initially dipped into negative territory within 6 hours of the absorption. However, subsequent market gains facilitated a recovery, ultimately resulting in positive reserve levels. In a scenario where the price of the collateral asset declined by 10% following absorption, the resulting Comet reserves would have been $-15,399.40.

| Scenario Type | Cumulative Value |

|---|---|

| Actual Scenario | $11,674.71 |

| 10 Percent Decrease | $-15,399.40 |

| 20 Percent Decrease | $-39,502.04 |

| 30 Percent Decrease | $-63,719.76 |

Hypothetical $1M Absorb Collateral Scenario

In this scenario, we apply the same assumptions used for the OP USDT Comet but adjust the collateral absorption amount to $1 million. As illustrated in the accompanying table and graph, the reserves generated from the liquidation would remain positive under historical market price conditions. However, the scenario reveals that reserves could have experienced substantial losses if prices had dropped further. Specifically, a 10% decline in asset prices from the point of absorption could have resulted in a reserve loss of approximately $87k.

| Scenario Type | Cumulative Value |

|---|---|

| Actual Scenario | $20,943.84 |

| 10 Percent Decrease | $-87,787.54 |

| 20 Percent Decrease | $-184,585.28 |

| 30 Percent Decrease | $-281,845.20 |

Hypothetical $5M Absorb Collateral Scenario

This scenario applies a collateral absorption amount of $5 million, a feasible figure given the $32 million in liquidations observed on Mainnet USDC Comet, particularly as these Comets scale. A 30% decline in asset prices from the point of absorption could result in a $1.4 million reduction in reserves. Such a significant loss would substantially deplete the base token reserves, potentially leading to elevated utilization rates and an increased risk of a liquidity crisis or bank run on the Comet.

| Scenario Type | Cumulative Value |

|---|---|

| Actual Scenario | $70,313.35 |

| 10 Percent Decrease | $-473,343.52 |

| 20 Percent Decrease | $-957,332.23 |

| 30 Percent Decrease | $-1,443,631.83 |

Compound’s Liquidator Ecosystem

As illustrated in the chart above, the lowest number of liquidator participants was observed on L2 chains, which corresponded with prolonged absorption times for collateral purchases. The minimal or non-existent presence of liquidators likely contributes to the outstanding collateral absorption in the BASE and Optimism (OP) Comets. The chart below presents a comparative analysis of liquidator participation during the same market downturn, revealing that the number of active liquidators on other networks is three times that of those in the BASE and Optimism Comets.

Gauntlet’s Call to Action

Gauntlet’s methodologies and simulations are predicated on the assumption of a robust liquidation ecosystem, wherein arbitrageurs actively seek profitable trading opportunities. Our models do not incorporate scenarios involving non-liquidator participants. Gauntlet recommends the next steps for the protocol and community:

- Gauntlet will evaluate risk mitigation recommendations for non-correlated Comets in the coming weeks to derisk Comets from inefficient liquidation performance.

- Gauntlet encourages community outreach efforts to ensure liquidators are informed about new Comets and arbitrage opportunities.

- Assistance from the community in contacting liquidators and MEV searchers to highlight potential profit opportunities would be invaluable. Gauntlet will also proactively reach out to relevant parties to help improve a healthy liquidation market. Gauntlet is already in communication with proactive community members who are working to solve the issue of liquidations on new chains and markets. Here is forum post with examples of a liquidator bot for Compound stakeholders.

- Gauntlet recommends the community re-evaluate the Liquidator Points functionality within Liquidations. The function tracks users who have executed absorb function by tallying liquidator “points” and gas the liquidator has spent. Gauntlet recommends the community evaluate utilizing this functionality to award those users to call the absorption function. A secondary consideration in our Market Downturn analysis involves the detection of delayed signals for triggering absorption processes.

Gauntlet will continue to monitor liquidation activities within the protocol and provide further insights on absorption and collateral purchase performance. Should these mechanisms continue to pose significant risks to the Comets, we may recommend reengineering the liquidation mechanism to enhance its effectiveness.

Next Steps

- Welcome any community feedback.