Simple Summary

The community has expressed interest in deprecating the v2 market. Recent Gauntlet recommendations have been aligned with this strategic initiative, with the execution of pausing of supply for v2 tail assets.

To further deprecate the v2 market, Gauntlet has the following goals in mind:

- Ensure enough borrowable USDC exists in v3 so that v2 users can migrate

- Limit poor UX for v2 users

As a first step in the deprecation plan, Gauntlet recommends the following changes:

- Decrease v3 utilization kink to 90%

- Increase v3 Annual Interest Rate Slope High parameters

- Allocate v2 rewards to v3 Ethereum USDC suppliers

- Increase v2 stablecoin reserve factors

We welcome community feedback and will create a poll to gauge community preferences on these options.

Analysis

Goal 1) Ensure enough borrowable USDC exists in v3

While deprecating v2, we want to ensure that users leaving v2 can migrate to v3.

In the past month, we are happy to see that the largest non-recursive v2 borrower with address 0xe84a061897afc2e7ff5fb7e3686717c528617487 has started to migrate towards Ethereum USDC.

In Ethereum USDC, this user supplies $53.78M WBTC and borrows $25.39M USDC.

In Compound v2, this user supplies $114.36M total collateral ($53.10M WETH, $43.63M WBTC, $17.63M BAT) and borrows $55.45M stablecoins ($53.95M USDC, $1.50M DAI).

Below are time series of this user’s supply and borrow balances in Ethereum USDC.

The Ethereum USDC Interest Rate proposal to reintroduce the kink at 95% and allocate rewards to USDC suppliers was executed on 7/17/23.

As seen above, utilization in Ethereum USDC has remained high since the proposal was executed, often above 95%, despite appealing Net Supply APR. While large v2 borrowers can still partially migrate to v3 at high utilizations, they have limited borrowable USDC. They are also less incentivized to borrow above the kink due to the resulting higher borrow APRs.

Below are some options to increase borrowable in USDC.

Option 1) Decrease v3 utilization kink to 90%

Pros

- Increased borrowable USDC at lower equilibrium utilization.

- Increased willingness for USDC suppliers to supply, knowing they have a greater chance to withdraw their USDC if equilibrium utilization is lower.

Cons

- Although decreased utilization yields more borrowable USDC, borrowers are empirically less likely to borrow past the kink at higher borrow APRs. In a way, this may result in less “feasibly borrowable” USDC.

- Less appealing equilibrium APRs.

Option 2) Increase v3 Annual Interest Rate Slope High parameters

Pros

- Minimizes time spent at high utilization, either by suppliers increasing supply at greater post-kink supply APRs, or by borrowers repaying at greater post-kink borrow APRs.

- Increased willingness for USDC suppliers to supply, knowing they:

- Have a greater chance to withdraw their USDC if equilibrium utilization is lower.

- Will receive higher supply APR during periods of high utilization.

Cons

- Less appealing for borrowers who are concerned about incurring high variable borrow APR.

Option 3) Increase v3 rewards to USDC suppliers

Currently, the v2 protocol distributes 444.8 daily COMP rewards, split evenly to UDSC suppliers/borrowers and DAI suppliers/borrowers. Given the current COMP price of $55, this amounts to ~$25k daily COMP rewards. We could migrate all these rewards to Ethereum USDC suppliers, increasing the Earn Distribution from 0.50% to 2.72%.

Pros

- Increases Net Supply APR, thereby incentivizing USDC suppliers.

Cons

- Expensive

Option 4) Increase v2 USDC reserve factor

Pros

- Incentivizes v2 USDC suppliers to migrate to v3.

Cons

-

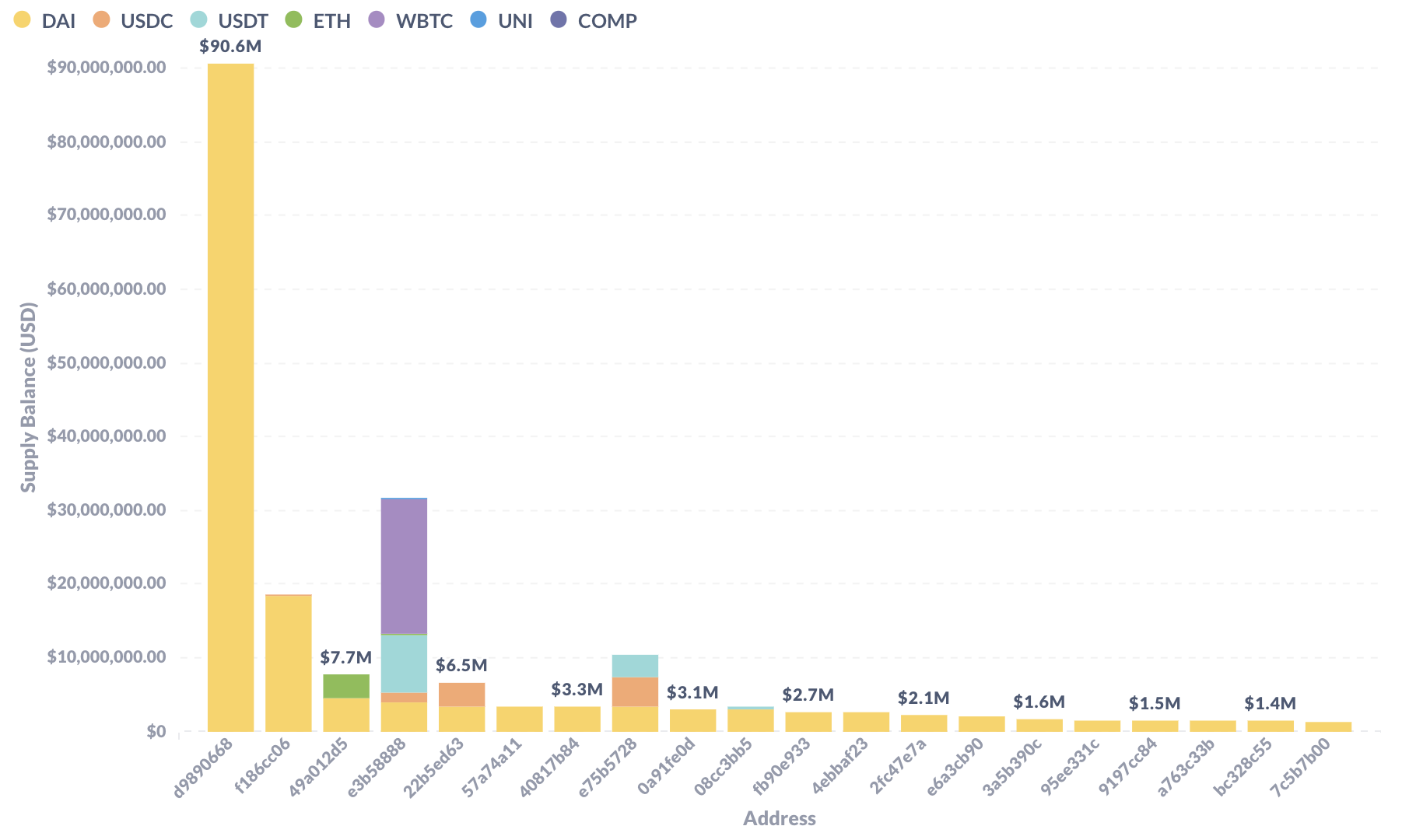

There are few remaining large non-recursive USDC suppliers in v2, as seen below:

Top USDC supplier entire supply positions

Top USDC supplier entire borrow positions

Goal 2) Limit poor UX for v2 users

Below are levers we can use when deprecating the v2 market and the corresponding immediate effects and impact to v2 UX:

| Parameter | Effects | UX rating (1 to 5, 5 = poorest UX) |

|---|---|---|

| Decrease collateral factors | Potential forced liquidations | 5 |

| Pause supply for WETH, WBTC, DAI, USDC, and USDT (the only remaining unpaused assets) | Inability to top up existing positions or open new positions | 4 |

| Decrease borrow caps | Limited ability to borrow in new or existing positions | 3 |

| Adjust IR Curves | Lower net supply APR, Higher net borrow APR | 2 |

| Decrease rewards | Lower net supply APR, Higher net borrow APR | 2 |

Decreasing collateral factors is arguably the most aggressive lever that could cause the largest volume to flee the protocol. Too many users fleeing the protocol at once may be problematic, given the limited borrowable USDC in v3. Additionally, reducing CF can also result in poor UX, as some users may experience forced liquidations.

Pausing supply for existing users may also result in poor UX, as the only way they could avoid liquidations in a market downturn would be to repay their borrows.

Recommendations

Given the tradeoffs of different options, Gauntlet’s recommends the first step in the v2 deprecation strategy should be to:

- Decrease v3 utilization kink to 90%

- Increase v3 Annual Interest Rate Slope High parameters

- Allocate v2 rewards to v3 Ethereum USDC suppliers

- Increase v2 stablecoin reserve factors

Afterward, depending on community preference, we can introduce more aggressive levers, including decreasing collateral factors and pausing supply.

Potential Risks

- Users may leave v2 and not migrate to v3, resulting in lower net TVL across all Compound markets

- As supply leaves v2, utilization may increase. The v2 max stablecoin borrow APRs are 32.50%, which are unlikely to cause any immediate forced liquidations. However, these high borrow APRs may result in a quick outflow from the protocol.

Next Steps

We welcome community feedback and will create a poll to gauge community preferences on these options.